There’s nothing in the Reserve Bank Act, or in the concept of central bank independence more generally, that says the treasurer can’t be as critical of the RBA as he likes. There’s a lot of silly hand-wringing about “inappropriateness” every time this happens. Our economists should not be so delicate. A government at war with its own money printer is a sign of the bank’s independence, rather than a lack of it.

But Jim Chalmers’ salvo against the RBA this close to an election is embarrassing and desperate. Foreshadowing the anaemic GDP growth figures released yesterday, the treasurer declared that the fault is all with the RBA: it is “smashing the economy” by keeping interest rates high to slow inflation.

It’s not unusual for governments to be frustrated when monetary policy contradicts their political strategy. It is unusual for a treasurer to so aggressively try to offload blame for sluggish growth onto a central bank whose governor he appointed and whose mandate and approach he endorsed less than a year ago.

The problem for the Albanese government is simple. There is a fundamental tension between the government’s election strategy (to relieve the pressure of inflation on household budgets through fiscal transfers and try to prop up the economy with government spending) and the RBA’s requirement to get inflation down — inflation that is exacerbated by the government’s fiscal transfers and expenditure. So we have had higher interest rates for longer while the Albanese government has tried to shield voters from the impact of those higher rates while keeping spending high.

Chalmers knows full well that monetary and fiscal policy can work against each other. Back during the global financial crisis, an internal government meeting between treasurer Wayne Swan, prime minister Kevin Rudd, treasury secretary Ken Henry, and “senior staff” specifically discussed how, if government spending increased, the RBA would likely keep interest rates higher than it would otherwise (I wrote about the implications of this meeting for ABC’s The Drumhere). Chalmers was Swan’s principal adviser when that meeting occurred.

If only the government and the RBA could row in the same direction. But the blame for policy divergence has to rest entirely with the government. RBA policy choices are strictly bounded by its legislative objectives and its extremely limited set of tools. Chalmers has a lot more discretion.

We might have some sympathy for Chalmers’ predicament. It must be galling to see other central banks starting to reduce rates. Voters always blame the elected government for a poor economy. They are right to. Ultimately it is Parliament that has the most tools to boost productivity and through that economic growth.

But there’s no time before the election to turn private sector growth around and there’s seemingly no appetite within the government to resolve the fiscal-monetary contradiction. Chalmers’ comments on Sunday were immediately following Anthony Albanese’s Saturday announcement of further “cost of living” relief in the form of increased rent assistance payments.

After the economic data this week, there’s a good chance that the RBA will change tack soon. But you can see what Chalmers is trying to do: shift blame onto the bank for the economy’s poor performance generally.

I started by observing that there’s nothing wrong, in principle, with the treasurer complaining about RBA policy. Yet this is a sensitive moment for the central bank. At the same time as Chalmers is accusing the bank of economic recklessness, he is also trying to finalise the overhaul of its governance, splitting the board into a monetary and governance committee. The treasurer wants this reform to be bipartisan. After this week’s events, the Coalition should insist that any reform and associated personnel choices wait until election season is over, whoever wins.

The arrest of the Telegram CEO Pavel Durov in France this week is extremely significant. It confirms that we are deep into the second crypto war, where governments are systematically seeking to prosecute developers of digital encryption tools because encryption frustrates state surveillance and control. While the first crypto war in the 1990s was led by the United States, this one is led jointly by the European Union — now its own regulatory superpower.

What these governments are insisting on, one criminal case at a time, is no less than unfettered surveillance over our entire digital lives.

Durov, a former Russian, now French citizen, was arrested in Paris on Saturday, and has now been indicted. You can read the French accusations here. They include complicity in drug possession and sale, fraud, child pornography and money laundering. These are extremely serious crimes — but note that the charge is complicity, not participation. The meaning of that word “complicity” seems to be revealed by the last three charges: Telegram has been providing users a “cryptology tool” unauthorised by French regulators.

In other words, the French claim is that Durov developed a tool — a chat program that allowed usersto turn on some privacy features — used by millions of people, and some small fraction of those millions used the tool for evil purposes. Durov is therefore complicit in that evil, not just morally but legally. This is an incredibly radical position. It is a charge we could lay at almost every piece of digital infrastructure that has been developed over the past half century, from Cloudflare to Microsoft Word to TCP/IP.

There have been suggestions (for example by the “disinformation analysts” cited by The New York Times this week) that Telegram’s lack of “content moderation” is the issue. There are enormous practical difficulties with having humans or even AI effectively moderate millions of private and small group chats. But the implication here seems to be that we ought to accept — even expect — that our devices and software are built for surveillance and control from the ground up: both the “responsible technology” crowd and law enforcement believe there ought to be a cop in every conversation.

It is true that Telegram has not always been a good actor in the privacy space, denigrating genuinely secure-by-design platforms like Signal while granting its own users only limited privacy protection. Telegram chats are not fully or always encrypted, which leaves users exposed to both state surveillance and non-state criminals. Wired magazine has documented how the Russian government has been able to track users down for their apparently private Telegram conversations. For that matter, it would not be surprising to learn that there are complex geopolitical games going on here between France and Russia.

But it would be easier to dismiss the claims made against Durov as particular to Telegram, or dependent on some specific action of Durov as an individual, if he was alone in being targeted as an accomplice for criminal acts simply because he developed privacy features for the digital economy.

The Netherlands have imprisoned the developer Alexey Pertsev for being responsible for the malicious use of a cryptocurrency privacy tool he developed, Tornado Cash. Again, Pertsev was not laundering money; he built a tool to protect every user’s privacy. The United States has arrested the developers of a Bitcoin privacy product, Samourai Wallet, also for facilitating money laundering.

The arrest of Durov suggests that the law enforcement dragnet is being widened from private financial transactions to private speech. If it is a crime to build privacy tools, there will be no privacy.

Published in Crikey. Part of a debate about whether taxpayers should fund journalism.

The case for subsidising journalism is weak. The case for subsidising journalism more than we already do is incredibly weak.

The government already directly pays for journalism through the ABC (1.1 billion in the 2022-23 budget) and SBS (316 million). With my colleague Sinclair Davidson I am famously sceptical that public broadcasting is a good idea. (Maybe infamously.) But put the argument for privatising the ABC and SBS aside. Policy choices do not exist in a vacuum. Any case for journalism subsidies should first explain why our already significant expenditure has failed, and whether there are any ways to reform our public broadcasters to more directly align with our policy goals. There is a lot the ABC and SBS do that isn’t journalism — would some of it be better redirected?

It is true that democracy relies on a thriving public sphere, of which news and journalism are critical parts. But on this count, Australian democracy doesn’t seem to be doing too badly. In the digital age, our problem as citizens and voters is not an information deficit but an information surplus — there is an enormous amount of online and offline content about the actions of the Australian government and civil society that we can consume. Digging through that content is the real challenge. Usually, we say that governments should subsidise things if the market underprovides for them. What is underprovided here? How should we measure it?

The real struggle is within media firms. Having lost their monopoly over advertising to a richer, more diverse, and more complex digital ecosystem, they find themselves competing to produce an extremely low-margin product while trying to support their legacy, high labour and production costs. I understand that the media industry has gone through 20 years of industrial pessimism. But at the same time, there are now senior journalists who have experienced nothing but disruption and have thrived within it. Too often policymakers confuse protecting established companies with supporting what they produce.

Practical considerations also undermine the case for journalism subsidies.

Almost any policy framework to subsidise journalism favours the large players that already dominate the Australian institutional media. Crikey has been arguing for a long time that News Corp pays less tax than it ought to. Guess who the biggest private beneficiaries of subsidised journalism are?

Maybe we can imagine a way to only favour the journalism we want, or to only favour smaller firms. But a policy framework that tried to discriminate against (say) the conservative talking shop ADH TV to only fund a left-leaning equivalent would merely invite the same government interference that the ABC labours under. A government unhappy with coverage could threaten to take away a media outlet’s privileges.

Government-subsidised journalism — whether through public broadcasting, tax breaks or direct subsidies — is fundamentally misconceived. It makes civil society the handmaiden of the state, rather than the other way around.

But in an important sense, the sort of policy rationalism I’m presenting here is beside the point. The question before policymakers is not whether subsidising journalism is a good use of taxpayer funds. The question is what to do with the Morrison government’s News Media Bargaining Code now that Meta is refusing to play ball.

The code is a legendarily outrageous example of rent-seeking in the history of Australian public policy. It is simply one sector using the government to directly extort money from another sector of the economy. And on the flimsiest pretence too: we have been asked to believe that allowing users to share news links with friends is somehow a violation of intellectual property.

The only “bargaining” that is going on here is between the media giants and the government. Meta and Google are the objects of the bargaining, not the participants.

The irony is that, if anything, the digital firms that are being targeted have been responsible for what has historically been the sharpest growth in the public sphere since the Gutenberg press. If democracy is first and foremost about citizen engagement, then they have been great for democracy.

Scratch the whole thing and start over. Media companies never had a natural right to advertising dollars and they have absolutely no right to funds forcibly extracted from companies in another sector. If we think the market is underproviding journalism then let’s see if our public broadcasters can spend their budgets better. At the very least, it is time to draw a line under this shameful, rent-seeking episode.

What happens when quantum computing is added to the digital economy?

The economics of quantum computing starts from a simple observation: in a world where search is cheaper, more search will be consumed. Quantum computing offers potentially dramatic increases in the ability to search through data. Searching through an unstructured list of 1,000,000 entries, a ‘classical’ computer would take 1,000,000 steps. For a mature quantum computer, the search would only require about 1,000 steps.

Bova et al. (2021) describe this capability generally as a potential advantage at solving combinatorics problems. The goal in combinatorics problems is often to search through all possible arrangements of a set of items to find a specific arrangement that meets certain criteria. While the cost of error correction or quantum architecture might erode the advantage quantum computers have in search, this is more likely to be an engineering hurdle to be overcome than a permanent constraint.

Economics focuses on exchange. To our knowledge no analysis of the economic impact of quantum computing has been focused on the effect that quantum computing has on the practice and process of exchange. Where there have been estimates of the economic benefits of quantum computing, those analyses have focused on the possibility that this technology might increase production through scientific discovery or by making production processes more efficient (for example by solving optimisation problems). So what impact will more search have on exchange?

In economics, search is a transaction cost (Stigler 1961, Roth 1982) that raises the cost of mutually beneficial exchange. Buyers have to search for potential sellers and vice versa. Unsurprisingly, much economic organisation is structured around reducing search costs. Indeed, it is the reduction of search costs that structures the digital platform economy. Multi-sided markets like eBay match buyers with sellers at global scale, allowing for trades to occur that would not be possible otherwise due to the high cost of search.

Quantum computing offers a massive reduction in this form of transactions cost. And all else being equal, we can expect that a massive reduction in search costs would have a correspondingly large effect on the structure of economic activity. For example, search costs are one reason that firms (and sub-firm economic agents like individuals) prefer to own resources rather than access them over the market. When you have your own asset, it is quicker to utilise that asset than seeking a market counterpart who will rent it to you.

Lowering search costs favours outsourcing rather than ownership (‘buy’ in the market, rather than ‘make’ inhouse). Lower search costs have a globalising effect — it allows economic actors to do more search — that is, explore a wider space for potential exchange. This has the effect of increasing the size of the market, which (as Adam Smith tells us), increases specialisation and the gains from trade. In this way, quantum computing powers economic growth.

Typically specialisation and globalisation increases the winner-take-all effect — outsized gains to economic actors at the top of their professions. However, a countervailing mechanism is that cheaper search also widens the opportunities to undercut superstar actors. This suggests an important implication of greater search on global inequality — it is easier to identify resources outside a local area. That should reduce rents and result in more producers (ie workers) receiving the marginal product of their labour as determined by global prices, rather than local prices. In this way, quantum computing drives economic efficiency.

Quantum and the digital stack

Of course other transactions costs (the cost of making the exchange, the cost of contract enforcement etc), can reduce the opportunities for faster search to disrupt existing patterns of economic activity. Here we argue that quantum is particularly effective in an environment of digital (or digitised) trade and production — in the domain of the information economy.

The process of digitisation is the process of creating more economic objects and through the use of distributed ledgers and digital twins, forming more and more precise property rights regimes. In Berg et al (2018), we explored one of the implications of this explosion in objects with precisely defined property rights. We argued that the increasingly precise and security digital property rights over objects would allow artificially intelligent agents to trade assets on behalf of their users, facilitating barter-like exchanges and allowing a greater variety of assets to be used as ‘money’. Key to achieving this goal is deep search across a vast matrix of assets, where the optimal path between two assets has to be calculated according to the pre-defined preferences not only of the agents making the exchange, but of each of the holders of the assets that form the paths.

This illuminates one of the ways in which quantum interacts with the web3 tech stack. While some quantum computation scientists have identified the opportunity for quantum to be used in AI training, we see the opportunity for quantum to be used by AI agents to search for exchange with other AI agents; an exchange theoretic rather than production-centric understanding of quantum’s contribution to the economy. The massive technological change we are experiencing is both cumulative and non-sequential — rapid developments in other parts of the tech stack further drive demand for the quantum compute. This is the digital quantum flywheel effect.

Compute as a commodity

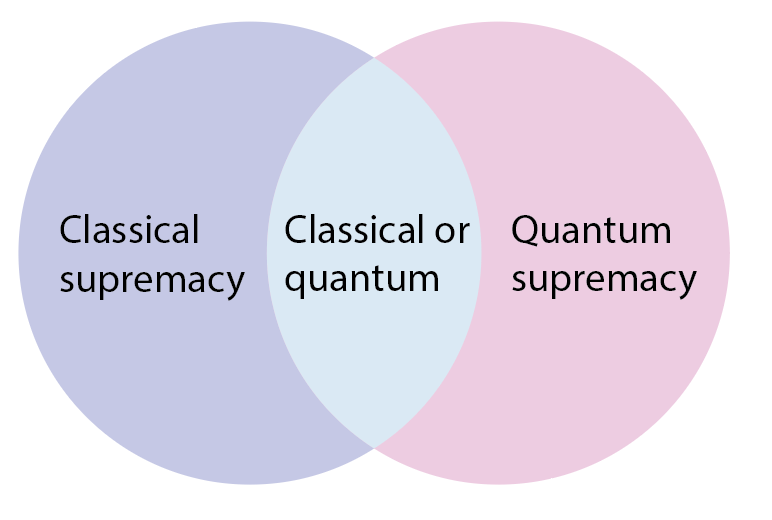

Compute is a commodity and follows the rules of commodity economics. Just as buyers of coal or electricity are ultimately buying the energy embodied in those goods, buyers of compute are ultimately buying a reduction in the time it takes to perform a computational task (Davies 2004). There are computational tasks where classical computers are superior (either cheaper or faster), where quantum computers are superior (or could be superior), and those where both quantum and classical computers can satisfy demand. Users of compute should be indifferent as to the origin of the compute they consume, but they have specific computational needs that they wish to perform subject to budget and time constraints. And they should be indifferent to the mixture of classical and quantum computing that best suits their needs and constraints.

This indifference between classical and quantum has significant consequences for how quantum computing is distributed between firms in the economy — and, indeed, between geopolitical powers. At this stage in the development of quantum computing, the major open question is how relatively large the space of computational tasks that are best suited for classical computing are versus that for quantum computing.

For computational tasks where classical computers dominate, compute is already massively decentralised — not just with multiple large cloud services (AWS, Google etc) but in the devices on our desks and in our pockets. There is no barrier to competition in classical compute, nor any risk of one geopolitical actor dominating. Where bottlenecks in classical compute emerge are in the production networks for semiconductor chips — a known problem with a known menu of policy stances and responses. Similarly, no such risk emerges around computational tasks where classical or quantum systems are equally suited.

The salient question is whether there will arise a natural monopoly in quantum compute? This could arise as a result of bottlenecks (say of scarce minerals, or caused by market structure as in the semiconductor chip industry), or as an outcome of competition in quantum computing development. As an example, one argument might be that as quantum compute power scales exponentially with the number of qubits then a geopolitical or economic actor that establishes a lead in qubit deployment could maintain that lead indefinitely due to compounding effects. This is a quantum takeoff analogous to the hypothesised ‘AI takeoff’ (see Bostrom 2014).

Several factors mitigate against this. The diversity of architectures for quantum computing being built suggests that the future is likely to be highly competitive; not merely between individual quantum compute systems but between classes of architectures (eg. superconducting, ion trap, photonics). While quantum compute research and development is very high cost, it is proceeding widely and with significant geographical dispersion. There are at least eight distinct major systems or architectures for quantum computing, seven of which have successfully performed basic computational tasks such as the control of qubits (see the survey by Bremmer et al 2024).

Nor is there any obvious concern that first-mover advantage implies competitive lock-in. Quantum compute is quite unlike AI safety scenarios, where ‘superintelligence’ or ‘foom’ is hypothesised to lead to a single monopolistic AI as a result of the superintelligence using its capabilities to 1) develop itself exponentially and 2) act to prevent competitors emerging. Quantum computing is and will be, for the long foreseeable future, a highly specialised toolset for particular tasks, not a general program that could pursue world domination either autonomously or under the direction of a bad actor.

One significant caveat to this analysis is that the capabilities of quantum compute might have downstream consequences for the economy, and this could . The exponential capabilities at factoring provided by quantum compute could undermine much of the cryptography that protects global commerce, and underlines the need for the development and deployment of post-quantum cryptography. We have argued elsewhere that the signals for the emergence of quantum supremacy in code breaking will emerge in the market prices of cryptocurrency (Rohde et al 2021). There is a significant risk mitigation task ahead of us to adopt post-quantum cryptography. It is a particularly difficult task because while the danger is concrete, the timeline for a quantum breakthrough is highly uncertain. Nonetheless, the task of migrating between cryptographic standards is akin to many other cybersecurity mitigations that have been performed in the digital economy, and while challenging should not be seen as existential.

Instead, the institutional economic view of quantum computing emphasises the possibilities of this new technology to radically grow the space for market exchange — particularly when we understand the possibility of quantum computing as co-developing alongside distributed ledgers, smart contracts (that is, decentralised digital assets) and artificial intelligence. Quantum computing lowers the cost and increases the performance of economic exchange across an exponentially growing ecosystem of digital property rights. It will be an important source of future economic value from better economic institutions.

References

Berg, Chris, Sinclair Davidson, and Jason Potts. ‘Beyond Money: Cryptocurrencies, Machine-Mediated Transactions and High-Frequency Hyperbarter’, 2018, 8.

Bremner, Michael, Simon Devitt, and Dr Eser Zerenturk. “Quantum Algorithms and Applications.” Office of the NSW Chief Scientist & Engineer, March 2024.

Bova, Francesco, Avi Goldfarb, and Roger G. Melko. ‘Commercial Applications of Quantum Computing’. EPJ Quantum Technology 8, no. 1 (December 2021): 1–13. https://doi.org/10.1140/epjqt/s40507-021-00091-1.

Rohde, Peter P, Vijay Mohan, Sinclair Davidson, Chris Berg, Darcy W. E. Allen, Gavin Brennen, and Jason Potts. “Quantum Crypto-Economics: Blockchain Prediction Markets for the Evolution of Quantum Technology,” 2021, 12.

Roth, Alvin E. ‘The Economics of Matching: Stability and Incentives’. Mathematics of Operations Research 7, no. 4 (1982): 617–28.

Stigler, George J. ‘The Economics of Information’. Journal of Political Economy 69, no. 3 (1961): 213–25.

World Economic Forum, 28 November 2022. Originally published here. With Justin Banon, Jason Potts and Sinclair Davidson.

The world economy is in the early stages of a profound transition from an industrial to a digital economy.

The industrial revolution began in a seemingly unpromising corner of northwest Europe in the early 1800s. It substituted machine power for animal and human power, organized around the factory system of economic production. Soon, it created the conditions to lift millions of humans from a subsistence economy into a world of abundance.

The digital economy began with similarly unpromising origins when Satoshi Nakomoto published his Bitcoin white paper to an obscure corner of the internet in late 2008. We call this the origin of Web3 now – with the first blockchain – but this revolution traces back decades as the slow economic application of scientific and military technologies of digital communication. The first wave of innovation was in computers, cryptography and inter-networking – Web1.

By the late 1990s, so-called “e-commerce” emerged as new companies, which soon became global platforms, built technologies that enabled people to find products, services and each other through new digital markets. That was Web2, the dot-com age of social media and tech giants.

But the actual age of digital economies was not down to these advances in information and communications technologies but to a very different type of innovation: the manufacture of trust. And blockchains industrialize trust.

Industrial economies industrialized economic production using physical innovations, such as steam engines and factories. Such institutional technologies organize people and machines into high production. What the steam engine did for industry, the trust engine will do for society. The fundamental factor of production that a digital economy economizes on is trust.

Blockchain is not a new tool. It is a new economic infrastructure that enables anyone, anywhere, to trust the underlying facts recorded in a blockchain, including identity, ownership and promises represented in smart contracts.

These economic facts are the base layer of any economy. They generally work well in small groups – a family, village or small firm – but the verification of these facts and monitoring of how they change becomes increasingly costly as economic activity scales up.

Layers of institutional solutions to trust problems have evolved over perhaps thousands of years. These are deep institutional layers – the rule of law, principles of democratic governance, independence of bureaucracy etc. Next, there are administrative layers containing organizational structures – the public corporation, non-profits, NGOs and similar technologies of cooperation. Then we have markets – institutions that facilitate exchange between humans.

It has been the ability to “truck, barter and exchange” over increasing larger markets that has catapulted prosperity to the levels now seen around the world.

Information technology augments our ability to interact with other people at all levels – economic, social and political. It has expanded our horizons. In the mid-1990s, retail went onto the internet. The late 1990s saw advertising on the internet. While the mid-2000s saw the news, information and friendship groups migrate to the internet. Since their advent in 2008, cryptocurrencies and natively digital financial assets have also come onto the internet. The last remaining challenge is to put real-world (physical) assets onto the internet.

The technology to do so already exists. Too many people think of non-fungible tokens (NFTs) as trivial JPEGs. But NFTs are not just collectable artworks; they are an ongoing experiment in the evolution of digital property rights. They can represent a certificate of ownership or be a digital twin of a real-world asset. They enable unique capital assets to become “computable,” that is, searchable, auditable and verifiable. In other words, they can be transacted in a digital market environment with a low cost of trust.

The internet of things can track real-world assets in real-time. Oracles can update blockchains regarding the whereabouts of physical assets being traded on digital markets. For example, anyone who has used parcel tracking over the past two years has seen an early version of this technology at work.

Over the past few years, people have been hard at work building all that is necessary to replicate real-world social infrastructure in a digital world. We now have money (stablecoins), assets (cryptocurrencies e.g. Bitcoin), property rights (NFTs) and general-purpose organizational forms (decentralized autonomous organizations (DAOs)). Intelligent people are designing dispute-resolution mechanisms using smart contracts. Others are developing mechanisms to link the physical and digital worlds (more) closely.

When will all this happen? The first-mover disadvantage associated with technological adoption has been overcome, mostly by everyone having to adopt new practices and technology simultaneously. Working, shopping and even entertaining online is now a well-understood concept. Digital connectedness is already an integral part of our lives. A technology that enhances that connectedness will have no difficulty in being accepted by most users.

It is very easy to imagine an interconnected world where citizens, consumers, investors and workers seamlessly live their lives transitioning between physical and digital planes at will before the decade concludes.

Such an economy is usefully described as a digital economy because that is the main technological innovation. And the source of economic value created is rightly thought of as the industrialization of trust, which Web3 technologies bring. But when the physical parts of the economy and the digital parts become completely and seamlessly join, this might well be better described as a “computable economy.” A computable economy has low-cost trust operating at global market scale.

The last part of this system that needs to fall into place is “computable capital.”

Now that we can tokenize all the world’s physical products and services into a common, interoperable format; list them within a single, public ledger; and enable market transactions with low cost of trust, which are governed by rules encoded within and enforced by the underlying substrate, what then?

Then, computable capital enables “programmable commerce,” but more than that – it enables what we might call a “turing-complete economy.”

The US government’s action against the blockchain privacy protocol Tornado Cash is an epoch-defining moment, not only for cryptocurrency but for the digital economy.

On Tuesday, the US Treasury Department placed sanctions on Tornado Cash, accusing it of facilitating the laundering of cryptocurrency worth $US7 billion ($10.06 billion) since 2019. Some $455 million of that is connected to a North Korean state-sponsored hacking group.

Even before I explain what Tornado Cash does, let’s make it clear: this is an extraordinary move by the US government. Sanctions of this kind are usually put on people – dictators, drug lords, terrorists and the like – or specific things owned by those people. (The US Treasury also sanctioned a number of individual cryptocurrency accounts, in just the same way as they do with bank accounts.)

But Tornado Cash isn’t a person. It is a piece of open-source software. The US government is sanctioning a tool, an algorithm, and penalising anyone who uses it, regardless of what they are using it for.

Tornado Cash is a privacy application built on top of the ethereum blockchain. It is useful because ethereum transactions are public and transparent; any observer can trace funds through the network. Blockchain explorer websites such as Etherscan make this possible for amateur sleuths, but there are big “chain analysis” firms that work with law enforcement that can link users and transactions incredibly easily.

Tornado Cash severs these links. Users can send their cryptocurrency tokens to Tornado Cash, where they are mixed with the tokens of other Tornado Cash users and hidden behind a state-of-the-art encryption technique called “zero knowledge proofs”. The user can then withdraw their funds to a clean ethereum account that cannot be traced to their original account.

Obviously, as the US government argues, there are bad reasons that people might want to use such a service. But there are also very good reasons why cryptocurrency users might want to protect their financial privacy – commercial reasons, political reasons, personal security, or even medical reasons. One mundane reason that investment firms used Tornado Cash was to prevent observers from copying their trades. A more serious reason is personal security. Wealthy cryptocurrency users need to be able to obscure their token holdings from hackers and extortionists.

Tornado Cash is a tool that can make these otherwise transparent blockchains more secure and more usable. No permission has to be sought from anyone to use Tornado Cash. The Treasury department has accused Tornado Cash of “laundering” more than $US7 billion, but that seems to be the total amount of funds that have used the service at all, not the funds that are connected to unlawful activity. There is no reason to believe that the Tornado Cash developers or community solicited the business of money launderers or North Korean hackers.

Now American citizens are banned from interacting with this open-source software at all. It is a clear statement from the world’s biggest economy that online privacy tools – not just specific users of those tools, but the tools themselves – are the targets of the state.

We’ve been here before. Cryptography was once a state monopoly, the exclusive domain of spies, diplomats and code breakers. Governments were alarmed when academics and computer scientists started building cryptography for public use. Martin Hellman, one of those who invented public key cryptography in the 1970s (along with Whitfield Diffie and Ralph Merkle), was warned by friends in the intelligence community his life was in danger as a result of his invention. In the so-called “crypto wars” of the 1990s, the US government tried to enforce export controls on cryptographic algorithms.

One of the arguments made during those political contests was that code was speech; as software is just text and lines of code, it should be protected by the same constitutional protections as other speech.

GitHub is a global depository for open-source software owned by Microsoft. Almost immediately after the Treasury sanctions were introduced this week, GitHub closed the accounts of Tornado Cash developers. Not only did this remove the project’s source code from the internet, GitHub and Microsoft were implicitly abandoning the long-fought principle that code needs to be protected as a form of free expression.

An underappreciated fact about the crypto wars is that if the US government had been able to successfully restrict or suppress the use of high-quality encryption, then the subsequent two decades of global digital commerce could not have occurred. Internet services simply would not have been secure enough. People such as Hellman, Diffie and Merkle are now celebrated for making online shopping possible.

We cannot have secure commerce without the ability to hide information with cryptography. By treating privacy tools as if they are prohibited weapons, the US Treasury is threatening the next generation of commercial and financial digital innovation.

How we understand where something comes from shapes where we take it, and I’m now convinced we’re thinking about the origins of blockchain wrong.

The typical introduction to blockchain and crypto for beginners – particularly non-technical beginners – gives Bitcoin a sort of immaculate conception. Satoshi Nakamoto suddenly appears with a fully formed protocol and disappears almost as suddenly. More sophisticated introductions will observe that Bitcoin is an assemblage of already-existing technologies and mechanics – peer to peer networking, public-key cryptography, the principle of database immutability, the hashcash proof of work mechanism, some hand-wavey notion of game theory – put together in a novel way. More sophisticated introductions again will walk through the excellent ‘Bitcoin’s academic pedigree’ paper by Arvind Narayanan and Jeremy Clark that guides readers through the scholarship that underpins those technologies.

This approach has many weaknesses. It makes it hard to explain proof-of-stake systems, for one. But what it really misses – what we fail to pass on to students and users of blockchain technology – is the sense of blockchain as a technology for social systems and economic coordination. Instead, it comes across much more like an example of clever engineering that gave us magic internet money. We cannot expect every new entrant or observer of the industry to be fully signed up to the vision of those that came before them. But it is our responsibility to explain that vision better.

Blockchains and crypto are the heirs of a long intellectual tradition building fault tolerant distributed systems using economic incentives. The problem this tradition seeks to solve is: how can we create reliable systems out of unreliable parts? In that simply stated form, this question serves not just as a mission statement for distributed systems engineering but for all of social science. In economics, for example, Peter Boettke and Peter Leeson have called for a ‘robust political economy’, or the creation of a political-economic system robust to the problems of information and incentives. In blockchain we see computer engineering converge with the frontiers of political economy. Each field is built on radically different assumptions but have come to the same answers.

So how can we tell an alternative origin story that takes beginners where they need to go? I see at least two historical strands, each of which take us down key moments in the history of computing.

The first starts with the design of fault tolerant systems shortly after the Second World War. Once electronic components and computers began to be deployed in environments with high needs for reliability (say, for fly-by-wire aircraft or the Apollo program) researchers turned their mind to how to ensure the failure of parts of a machine did not lead to critical failure of the whole machine. The answer was instinctively obvious: add backups (that is, multiple redundant components) and have what John von Neumann in 1956 called a ‘restoring organ’ combine their multiple outputs into a single output that can be used for decision-making.

But this creates a whole new problem: how should the restoring organ reconcile those components’ data if they start to diverge from each other? How will the restoring organ know which component failed? One solution was to have the restoring organ treat each component’s output as a ‘vote’ about the true state of the world. Here, already, we can see the social science and computer science working in parallel: Duncan Black’s classic study of voting in democracies, The Theory of Committees and Elections was published just two years after von Neumann’s presentation of the restoring organ tallying up the votes of its constituents.

The restoring organ was a single, central entity that collated the votes and produced an answer. But in the distributed systems that started to dominate the research on fault tolerance through the 1970s and 1980s there could not be a single restoring organ – the system would have come to consensus as a whole. The famous 1982 paper ‘The Byzantine Generals’ Problem’ paper by Leslie Lamport, Robert Shostak and Marshall Peace (another of the half-taught and quarter-understood parts of the origins of blockchain canon) addresses this research agenda by asking how many voting components are needed for consensus in the presence of faulty – malicious – components. One of their insights was cryptographically unforgeable signatures makes the communication of information (‘orders’) much simplifies the problem.

The generation of byzantine fault tolerant distributed consensus algorithms that were built during the 1990s – most prominently Lamport’s Paxos and the later Raft – now underpin much of global internet and commerce infrastructure.

Satoshi’s innovation was to make the distributed agreement system permissionless – more precisely, to join the network as a message-passer or validator (miner) does not require the agreement of all other validators. To use the Byzantine generals’ metaphor, now anyone can become a general.

That permissionlessness gives it a resilience against attack that the byzantine fault tolerant systems of the 1990s and 2000s were never built for. Google’s distributed system is resilient against a natural disaster, but not a state attack that targets the permissioning system that Google as a corporate entity oversees. Modern proof-of-stake systems such as Tendermint and Ethereum’s Casper are an evolutionary step that connects Bitcoin’s permissionlessness with decades of knowledge of fault tolerant distributed systems.

This is only a partial story. We still need the second strand: the introduction of economics and markets into computer science and engineering.

Returning to the history of computing’s earliest days, the institutions that hosted the large expensive machines of the 1950s and 1960s needed to manage the demand for those machines. Many institutions used sign-up sheets, some even had dedicated human dispatchers to coordinate and manage a queue. Timesharing systems tried to spread the load on the machine so multiple users could work at the same time.

It was not long before some researchers realised that sharing time on a machine was fundamentally a resource allocation problem that could be tackled by with relative prices. By the late 1960s Harvard University was using a daily auction to reserve space on their PDP-1 machine using a local funny money that was issued and reissued each day.

As the industry shifted from a many-users, one-computer structure to a many-users, many-distributed-computers structure, the computer science literature started to investigate the allocation of resources between machines. Researchers stretched for the appropriate metaphor: were distributed systems like organisations? Or were they like separate entities tied together by contracts? Or were they like markets?

In the 1988 Agoric Open Systems papers, Mark S. Miller and K. Eric Drexler argued not simply for the use of prices in computational resource allocation but to reimagine distributed systems as a full-blown Hayekian catallaxy, where computational objects have ‘property rights’ and compensate each other for access to resources. (Full disclosure: I am an advisor to Agoric, Miller’s current project.) As they noted, one missing but necessary piece for the realisation of this vision was the exchange infrastructure that would provide an accounting and currency layer without the need for a third party such as a bank. This, obviously, is what Bitcoin (and indeed its immediate predecessors) sought to provide.

We sometimes call Bitcoin the first successful fully-native, fully-digital money, but skip over why that is important. Cryptocurrencies don’t just allow for censorship-free exchange. They radically expand the number of exchange that can occur – not just between people but between machines. Every object in a distributed system, all the way up and down the technology stack, has an economic role and can form distinctly economic relationships. We see this vision in its maturity in the complex economics of resource allocation within blockchain networks.

Any origin story is necessary simplified, and the origin story I have proposed here skips over many key sources of the technology that is now blockchain: cryptography, the history and pre-history of smart contracts, and of course the cypherpunk community from which Bitcoin itself emerged. But I believe this narrative places us on a much sounder footing to talk about the long term social and economic relevance of blockchain.

As Sinclair Davidson, Jason Potts and I have argued elsewhere, blockchains are an institutional technology. They allow us to coordinate economic activity in radically different ways, taking advantage of the global-first, trust-minimised nature of this distributed system to create new types of contracts, exchanges, organisations, and communities. The scale of this vision is clearest when we compare it with what came before.

Consider, for instance, the use of prices for allocating computer time. The early uses of prices were either to recoup the cost of operation for machines, or as an alternative to queuing, allowing users to signal the highest value use of scarce resources. But prices in real-world markets do a lot more than that. By concentrating dispersed information about preferences they inspire creation – they incentivise people to bring more resources to market, and to invent new services and methods of production that might earn super-normal returns. Prices helped ration access to Harvard’s PDP-1, but could not inspire the PDP-1 to grow itself more capacity.

The Austrian economist Ludwig von Mises wrote that “the capitalist system is not a managerial system; it is an entrepreneurial system”. The market that is blockchain does not efficiently allocate resources across a distributed system but instead has propelled an explosion of entrepreneurial energy that is speculative and chaotic but above all innovative. The blockchain economy grows and contracts, shaping and reshaping just like a real economy. It is not simply a fixed network with nodes and connections. It is a market: it evolves.

We’ve of course seen evolving networks in computation before. The internet itself is a network – a web that is constantly changing. And you could argue that the ecosystem of open-source software that allows developers to layer and combine small, shared software components into complex systems looks a lot like an evolutionary system. Neither of these directly use the price system for coordination. They are poorer for it. The economic needs of internet growth has encouraged the development of a few small and concentrated firms while the economic needs of open-source are chronically under-supplied. To realise the potential of distributed computational networks we need the tools of an economy: property rights and a native means of exchange.

Networks can fail for many reasons: nodes might crash, might fail to send or receive messages correctly, their responses might be delayed longer than the network can tolerate, they might report incorrect information to the rest of the network. Human social systems can fail when information is not available where and when it is needed, or if incentive structures favour anti-social rather than pro-social behaviours.

As a 1971 survey of the domain of fault tolerant computing noted “The discipline of fault-tolerant computing would be unnecessary if computer hardware and programs would always behave in perfect agreement with the designer’s or programmer’s intentions”. Blockchains make the joint missions of economics and computer science stark: how to build reliable systems out of unreliable parts.

The blockchain and defi sector should understand more about how real world grant giving bodies function. Nowhere is this clearer than in the recent debate about UniSwap and its new $20 million Defi Education Fund.

In the real world, grant giving is a lot like venture finance. It is an entrepreneurial activity involving the discovery of new information, new opportunities, and new ideas. It helps realise those opportunities and ideas and is rewarded for doing so.

The fact that grants are done with a for-purpose goal while venture finance is done with a for-profit goal only makes a difference at the margin. The best grant giving bodies in the world work very hard to ensure that the custodians of funds have incentives tightly aligned to the overall objectives of the body. Some even use external independent auditors to see whether grants align to objectives, and penalise the program’s management if they do not. These rules bind the grant makers, allowing the grant seekers to innovate and discover how best to achieve the programs objectives.

Admittedly, it can be sometimes hard to see the entrepreneurial and discovery nature of grant programs. Academic research grants tend to be highly bureaucratic processes with layers of committees and appointed experts collating and judging grant proposals at arms-length from the funders.

But ultimately this bureaucracy has a purpose. Those systems of rules might seem inefficient, but they have been designed to align the dispersal of funds with the objectives of the fund. In the case of the Australian Research Council, all those committees are intended to fulfil the objectives of the Department of Education’s scientific mandate through discovery and investment. (Let’s not get hung up about how effective these government programs are.)

At the other end of the spectrum is Tyler Cowen’s Emergent Ventures grant program, where almost all decision-making is Cowen’s judgement. But this too is a structure designed to align objectives with fund dispersal. The objectives of the fund are to allow Cowen to use his knowledge to support “high-risk, high-reward ideas that advance prosperity, opportunity, and wellbeing” — and by all accounts the program is an incredible success.

Two approaches to defi grants

Right now we broadly have two models of grant giving in the defi space. The first is small centralised grant committees. These tend to be small groups of authoritative community leaders with near absolute control of large treasuries assessing and granting funds to desirable projects. These leaders may be elected or appointed, but either way they are using their authority in the community to legitimate their decisions. They may have a deep understanding of their ecosystem and its funding needs. An obvious problem with this is the risk that committee leaders opportunistically fund projects based on personal relationships, rather than ecosystem value.

The alternative model — and the most common one — is putting all grant proposals up to a vote of all relevant stakeholders, that is, holders of a governance token. Designing structures for effective collective decision-making is one of the hardest problems in political science. It is no surprise that some decision-making in the nascent blockchain governance world have been controversial.

But there’s a fundamental problem with this democratic model to grant making: it makes very little sense to believe that a full distributed democratic community can make the sort of entrepreneurial decisions that we expect from both venture finance and grant giving bodies themselves. Why would we expect a diverse, pseudonymous community of governance token holders to coordinate around extremely uncertain entrepreneurial decisions?

Throwing every proposal to a mass vote is the worst of all worlds. First, every proposal ultimately becomes a public vote about the objectives of the program itself. Should the treasury’s funds be used for marketing, or research, or to build new infrastructure? Grant recipients, and the ecosystem that relies on them, are left with inconsistency and unpredictability.

Second, there is little reason to believe that a mass vote will reveal the best investments. Highly decentralised voting may protect against opportunism, but it isn’t likely to surface information about entrepreneurial investment opportunities — exactly what is needed for successful grant-giving. This precise information-revelation problem is the motivation and intuition between mechanisms such as quadratic funding, futarchy, and commitment voting.

A better grant program design

This is a solvable problem. Treasuries should give budgets to individual ‘philanthropists’. Those philanthropists then make entrepreneurial investments to align the compensation of those entrepreneurs with the success of their invested projects.

The full set of tokenholders sets the objective of the grant program, or an individual round. These objectives would shift as a given ecosystem and the broader industry develops — for instance from funding oracle feeds, to bridging infrastructure, to policy change. Grants are broken into funding rounds. The length of those rounds, say a year or two, must be long enough that there are observable outcomes from grant projects. Rounds could be sequential or overlap.

Each round, a set of philanthropists (say, five) are chosen (elected or appointed) and given discrete budgets. The number of philanthropists for a given round could also be decided by all tokenholders.

Once the funds are dispersed to each philanthropist, they run separate and independent grant programs. They must have credible autonomy: with their own rules, their own application processes, and their own interpretation of the objectives of the overall grant program.

At the end of the round, the full set of tokenholders rank each of the five philanthropists according to how successful (how much value was added, how closely they aligned to objectives) their grants were. The philanthropists are compensated for their work based on that ranking, with the top-ranked getting the most reward.

In this way the grants program is designed to both fund projects, and to incentivise decision-making philanthropists to do a good job.

Our proposal drives the same sort of competitive, entrepreneurial energy that we see in venture finance into defi grant distribution.

Through grant program design we can encourage effective decision-making through feedback loops, while maintaining decentralisation (the risk that philanthropists will behave badly is limited to the length of a grant round) and giving philanthropists a personal stake in the success of the grants that they have distributed (encouraging them to support and shepherd them to fruition).

Grant program design matters a lot

It might be easy to dismiss grant program design as a sideshow in the blockchain industry, marginally interesting but ultimately not a central part of the success of any particular protocol. It would be wrong to do so.

Analogies in blockchain are difficult. But if DAOs are like corporations, then grant programs are how they do internal capital allocation — and as Alfred D. Chandler Jr. has shown, internal capital allocation has determined the shape of global capitalism. Alternatively, if blockchain ecosystems are like countries with governments, then when we talk about grant programs we’re talking about public finance — they are how we pay for public goods and deploy scarce resources in a democratic context.

Ultimately, the sustainability and robustness blockchain ecosystems require effective use of resources. The success of grant programs will form a critical part of the success of blockchain and dapp protocols. They should seek to harness the same entrepreneurial energy and effort that has driven the rest of the blockchain industry.

The COVID-19 pandemic is both a public health crisis, and a digital technology accelerant. Pre-pandemic, our economic and social activities were done predominantly in cities. We connected and we innovated in these centralised locations.

But then a global pandemic struck. We were forced to shop, study and socialise in a distributed way online. This shock had an immediate impact on our cities, with visceral images of closed businesses and silent streets.

Even after COVID-19 dissipates, the widespread digital adoption that the pandemic brought about means that we are not snapping back to pre-pandemic life.

The world we are entering is hybrid. It is both analogue and digital, existing in both regions and cities. Understanding the transition is critical because cities are one of our truly great inventions. They enable us to trade, to collaborate, and to innovate. In other words, cities aggregate economic activity.

The Digital CBD project is a large-scale research project that asks: what happens when that activity suddenly disaggregates? What happens to the city and its suburbs? What happens to the businesses that have clustered around the CBD? What infrastructure do we need for a hybrid digital city? What policy changes will be needed to enable firms and citizens to adapt?

Forced digital adoption

This global pandemic happened at a critical time. Many economies were already transitioning from an industrial to a digital economy. Communications technologies had touched almost every business. Digital platforms were commonly used to engage socially and commercially. But the use of these technologies was not yet at the core of our businesses, it sat on the sidelines. We were only on the cusp of a digital economy.

Then COVID-19 forced deep, coordinated, multi-sector and rapid adoption of digital technologies. The coordination failures and regulatory barriers that had previously held us back were wiped away. We swapped meeting rooms for conference calls, cash for credit cards, pens-and-paper for digital signatures. There had been a desire for these changes for a long time.

These changes make even more frontier technologies suddenly come into view. Blockchains, artificial intelligence, smart contracts, the internet of things and cybersecurity technologies are now more viable because of this base-level digital adoption.

Importantly, this suite of new technologies doesn’t just augment and improve the productivity of existing organisations, they make new organisational forms possible. It changes the structure of the economy itself.

Discovering our digital CBD

Post-pandemic, parts of our life and work will return to past practices. Some offices will reopen, requiring staff to return to rebuild morale and culture. And those people will also flood back into CBD shops, bars and restaurants. They will, as all flourishing cities encourage, meet and innovate.

But of course some businesses will relish their new-found productivity benefits – and some workers will guard the lifestyle benefits of working from home. Many firms will never fully reopen their offices and will brag about their remote-work dynamic culture.

The potential implications for cities, however, are more complex. Cities will fundamentally have different patterns of specialisation and trade than a pre-pandemic economy. Those new patterns are enabled by a suite of decentralised technologies, including blockchains and smart contracts, that were already disrupting how we organise our society.

We can now organise economic activity in new ways. CBDs have historically housed large, hierarchical industrial-era companies. As we have written elsewhere, decentralised infrastructure enables new types of organisational forms to emerge. Blockchains industrialise trust and shift economic activities towards decentralised networks.

How do these new types of industrial organisation change the way that we work, and the location of physical infrastructure? What are the policy changes necessary to enable these new organisations to flourish in particular jurisdictions?

Economies and cities are fundamentally networks of supply chains, and that infrastructure is turning digital too. The pandemic has accelerated the transition to digital trade infrastructure that provides more trusted and granulated information about goods as they move. How can we ensure that these digital supply chains are resilient to future shocks? What opportunity is there for regions to become a digital trade hub?

Another impact of digital technology is that labour markets just became more global. The acquisition of talented labour is no longer bounded by physical distance. Our collaborations are structured around timezones, rather than geography.

Labour market dynamism presents unique opportunities, but will also require secure infrastructure both to validate credentials and to facilitate ongoing productivity. How can Melbourne, a world-class cluster of universities, place itself for this new environment?

A research and a policy problem

Building a digital CBD is fundamentally an entrepreneurial problem—a problem of discovering what these new digital ways of coordinating and collaborating look like. Our Digital CBD research program contributes to this challenge with insights from economics, law, political science, finance, accounting and more. We aim to use this interdisciplinary research base to make policy recommendations that help our digital CBD to flourish.

With Darcy Allen, Sinclair Davidson, Trent MacDonald and Jason Potts. Originally a Medium post.

Blockchains are institutional technologies made of rules (e.g. consensus mechanisms, issuance schedules). Different rule combinations are entrepreneurially created to achieve some objectives (e.g. security, composability). But the design of blockchains, like all institutions, must occur under ongoing uncertainty. Perhaps a protocol bug is discovered, a dapp is hacked, treasury is stolen, or transaction volumes surge because of digital collectible cats. What then? Blockchain communities evolve and adapt. They must change their rules (e.g. protocol security upgrades, rolling back the chain) and make other collective decisions (e.g. changing parameters such as interest rates, voting for validators, or allocating treasury funds).

Blockchain governance mechanisms exist to aid decentralised evolution. Governance mechanisms include online forums, informal polls, formal improvement processes, and on-chain voting mechanisms. Each of these individual mechanisms — let alone their interactions — are poorly understood. They are often described through sometimes-useful but imperfect analogies to other institutional systems with deeper histories (e.g. representative democracy). This is not a robust way to design the decentralised digital economy. It is necessary to develop a shared language, and understanding, of blockchain governance. That is, a grammar of rules that can describe the entire possible scope of blockchain governance rules, and their relationships, in an analytically consistent way.

A starting point for the development of this shared language and understanding is a methodology and rule classification system developed by 2009 economics Nobel Laureate Elinor Ostrom to study other complex, nested institutional systems. We propose an empirical project that seeks conceptual clarity in blockchain governance rules and how they interact. We call this project Ostrom-Complete Governance.

The common approach to blockchain governance design has been highly experimental — relying very much on trial and error. This is a feature, not a bug. Blockchains are not only ecosystems that require governance, but the technology itself can open new ways to make group decisions. While being in need of governance, blockchain technology can also disrupt governance. Through lower costs of institutional entrepreneurship, blockchains enable rapid testing of new types of governance — such as quadratic voting, commitment voting and conviction voting — that were previously too costly to implement at scale. We aren’t just trying to govern fast-paced decentralised technology ecosystems, we are using that same technology for its own governance.

This experimental design challenge has been compounded by an ethos and commitment to decentralisation. That decentralisation suggests the need for a wide range of stakeholders with different decision rights and inputs into collective choices. The lifecycle of a blockchain exacerbates this problem: through bootstrapping a blockchain ecosystem can see a rapidly shifting stakeholder group with different incentives and desires. Different blockchain governance mechanisms are variously effective in different stages of blockchain development. Blockchains, and their governance, begin relatively centralised (with small teams of developers), but projects commonly attempt to credibly commit to rule changes towards a system of decentralised governance.

Many of these governance experiments and efforts have been developed through analogy or reference to existing organisational forms. We have sought to explain and design this curious new technology by looking at institutional forms we know well, such as representative democracy or corporate governance. Scholars have looked to existing familiar literature such as corporate governance, information technology governance, information governance, and of course political constitutional governance. But blockchains are not easily categorised as nation states, commons, clubs, or firms. They are a new institutional species that has features of each of these well-known institutional forms.

An analogising approach might be effective to design the very first experiments in blockchain governance. But as the industry matures, a new and more effective and robust approach is necessary. We now have vast empirical data of blockchain governance. We have hundreds, if not thousands, of blockchain governance mechanisms, and some evidence of their outcomes and effects. These are the empirical foundations for a deeper understanding of blockchain governance — one that embraces the institutional diversity of blockchain ecosystems, and dissects its parts using a rigorous and consistent methodology.

Embracing blockchain institutional diversity

Our understanding of blockchain governance should not flatten or obscure away from its complexity. Blockchains are polycentric systems, with many overlapping and nested centres of decision making. Even with equally-weighted one-token-one-vote blockchain systems, those systems are nested within other processes, such as a github proposal process and the subsequent execution of upgrades. It is a mistake to flatten these nested layers, or to assume some layers are static.

Economics Nobel LaureateElinorOstrom and her colleagues studied thousands of complex polycentric systems of community governance. Their focus was on understanding how groups come together to collectively manage shared resources (e.g. fisheries and irrigation systems) through systems of rules. This research program has since studied a wide range of commons including culture, knowledge and innovation. This research has been somewhat popular for blockchain entrepreneurs, in particular through using the succinct design principles (e.g. ‘clearly defined boundaries’ and ‘graduated sanctions’) of robust commons to inform blockchain design. Commons’ design principles can help us to analyse blockchain governance — including whether blockchains are “Ostrom-Compliant” or at least to find some points of reference to begin our search for better designs.

But beginning with the commons design principles has some limitations. It means we are once again beginning blockchain governance design by analogy (that blockchains are commons), rather than understanding blockchains as a novel institutional form. In some key respects blockchains resemble commons — perhaps we can understand, for instance, the security of the network as a common pool resource — but they also have features of states, firms, and clubs. We should therefore not expect that the design principles developed for common pool resources and common property regimes are directly transferable to blockchain governance.

Beginning with Ostrom’s design principles begins with the output of that research program, rather than applying the underlying methodology that led to that output. The principles were discovered as a meta-analysis of the study of thousands of different institutional rule systems. A deep blockchain-specific understanding must emerge from empirical analysis of existing systems.

We propose that while Ostrom’s design principles may not be applicable, a less-appreciated underlying methodology developed in her research is. In her empirical journey, Ostrom and colleagues at the Bloomington School developed a detailed methodological approach and rule classification system. While that system was developed to dissect the institutional complexity of the commons, it can also be used to study and achieve conceptual clarity in blockchain governance.

The Institutional Analysis and Development (IAD) framework and the corresponding rule classification system, is an effective method for deep observation and classification of blockchain governance. Utilising this approach we can understand blockchains as a series of different nested and related ‘action arenas’ (e.g. consensus process, a protocol upgrade, a DAO vote) where different actors engage, coordinate and compete under sets of rules. Each of these different action arenas have different participants (e.g. token holders), different positions (e.g. delegated node), and different incentives (e.g. to be slashed), which are constrained and enabled by rules.

Once we have identified the action arenas of a blockchain we can start to dissect the rules of that action arena. Ostrom’s 2005 book, Understanding Institutional Diversity, provides a detailed classification of rules classification that we can use for blockchain governance, including:

position rules on what different positions participants can hold in a given governance choice (e.g. governance token holder, core developer, founder, investor)

boundary rules on how participants can or cannot take part in governance (e.g. staked tokens required to vote, transaction fees, delegated rights)

choice rules on the different options available to different positions (e.g. proposing an upgrade, voting yes or no, delegating or selling votes)

aggregation rules on how inputs to governance are aggregated into a collective choice (e.g. one-token-one-vote, quadratic voting, weighting for different classes of nodes).

These rules matter because they change the way that participants interact (e.g. how or whether they vote) and therefore change the patterns that emerge from repeated governance processes (e.g. low voter turnout, voting deadlocks, wild token fluctuations). There have been somestudies that have utilised the broad IAD framework and commons research insights to blockchain governance, but there has been no deep empirical analysis of the rule systems of blockchains using the underlying classification system.

The opportunity

Today the key constraint in advancing blockchain governance is the lack of a standard language of rules with which to describe and map governance. Today in blockchain whitepapers these necessary rules are described in a vast array of different formats, with different underlying meanings. That hinders our capacity to compare and analyse blockchain governance systems, but can be remedied through applying and adopting the same foundational grammar. Developing a blockchain governance grammar is fundamentally an empirical exercise of observing and classifying blockchain ecosystems as they are, rather than imposing external design rules onto them. This approach doesn’t rely on analogy to other institutions, and is robust to new blockchain ecosystem-specific language and new experimental governance structures.

Rather than broadly describing classes of blockchain governance (e.g., proof-of-work versus proof-of-stake versus delegated-proof-of-stake) our approach begins with a common set of rules. All consensus processes have sets of boundary rules (who can propose a block? how is the block-proposer selected?), choice rules (what decisions do block-proposers make, such as the ordering of transactions?), incentives (what is the cost of proposing a bad block? what is the reward for proposing a block), and so on. For voting structures, we can also examine boundary rules (who can vote?), position rules (how can a voter get a governance token?) choice rules (can voters delegate? who can they delegate to?) and aggregation rules (are vote weights symmetrical? is there a quorum?).

We can begin to map and compare different blockchain governance systems utilising this common language. All blockchain governance has this underlying language, even if today that grammar isn’t explicitly discussed. The output of this exercise is not simply a series of detailed case studies of blockchain governance, it is detailed case studies in a consistent grammar. That grammar — an Ostrom-Complete Grammar — enables us to define and describe any possible blockchain governance structure. This can ultimately be leveraged to build new complete governance toolkits, as the basis for simulations, and to design and describe blockchain governance innovations.