Submission to House of Representatives Inquiry into Australian Agriculture in Southeast Asian Markets, with Darcy WE Allen and Aaron M Lane

The core of our submission is to emphasise the importance of digital economic infrastructure (e.g. identity systems, payments, traceability) for trade and economic development. This digital infrastructure can not only lower costs to facilitate more trade, but also is a critical mechanism by which Australian agriculture can continue to develop a trusted premium market positioning in the region.

Available at arXiv. With Joshua Tan, Tara Merk, Sarah Hubbard, Eliza R. Oak, Helena Rong, Joni Pirovich, Ellie Rennie, Rolf Hoefer, Michael Zargham, Jason Potts, Reuben Youngblom, Primavera De Filippi, Seth Frey, Jeff Strnad, Morshed Mannan, Kelsie Nabben, Silke Noa, Elrifai, Jake Hartnell, Benjamin Mako Hill, Tobin South, Ryan L. Thomas, Jonathan Dotan, Ariana Spring, Alexia Maddox, Woojin Lim, Kevin Owocki, Ari Juels, and Dan Boneh.

Abstract: Decentralized autonomous organizations (DAOs) are a new, rapidly growing class of organizations governed by smart contracts. Here we describe how researchers can contribute to the emerging science of DAOs and other digitally-constituted organizations. From granular privacy primitives to mechanism designs to model laws, we identify high-impact problems in the DAO ecosystem where existing gaps might be tackled through a new data set or by applying tools and ideas from existing research fields such as political science, computer science, economics, law, and organizational science. Our recommendations encompass exciting research questions as well as promising business opportunities. We call on the wider research community to join the global effort to invent the next generation of organizations.

What happens when quantum computing is added to the digital economy?

The economics of quantum computing starts from a simple observation: in a world where search is cheaper, more search will be consumed. Quantum computing offers potentially dramatic increases in the ability to search through data. Searching through an unstructured list of 1,000,000 entries, a ‘classical’ computer would take 1,000,000 steps. For a mature quantum computer, the search would only require about 1,000 steps.

Bova et al. (2021) describe this capability generally as a potential advantage at solving combinatorics problems. The goal in combinatorics problems is often to search through all possible arrangements of a set of items to find a specific arrangement that meets certain criteria. While the cost of error correction or quantum architecture might erode the advantage quantum computers have in search, this is more likely to be an engineering hurdle to be overcome than a permanent constraint.

Economics focuses on exchange. To our knowledge no analysis of the economic impact of quantum computing has been focused on the effect that quantum computing has on the practice and process of exchange. Where there have been estimates of the economic benefits of quantum computing, those analyses have focused on the possibility that this technology might increase production through scientific discovery or by making production processes more efficient (for example by solving optimisation problems). So what impact will more search have on exchange?

In economics, search is a transaction cost (Stigler 1961, Roth 1982) that raises the cost of mutually beneficial exchange. Buyers have to search for potential sellers and vice versa. Unsurprisingly, much economic organisation is structured around reducing search costs. Indeed, it is the reduction of search costs that structures the digital platform economy. Multi-sided markets like eBay match buyers with sellers at global scale, allowing for trades to occur that would not be possible otherwise due to the high cost of search.

Quantum computing offers a massive reduction in this form of transactions cost. And all else being equal, we can expect that a massive reduction in search costs would have a correspondingly large effect on the structure of economic activity. For example, search costs are one reason that firms (and sub-firm economic agents like individuals) prefer to own resources rather than access them over the market. When you have your own asset, it is quicker to utilise that asset than seeking a market counterpart who will rent it to you.

Lowering search costs favours outsourcing rather than ownership (‘buy’ in the market, rather than ‘make’ inhouse). Lower search costs have a globalising effect — it allows economic actors to do more search — that is, explore a wider space for potential exchange. This has the effect of increasing the size of the market, which (as Adam Smith tells us), increases specialisation and the gains from trade. In this way, quantum computing powers economic growth.

Typically specialisation and globalisation increases the winner-take-all effect — outsized gains to economic actors at the top of their professions. However, a countervailing mechanism is that cheaper search also widens the opportunities to undercut superstar actors. This suggests an important implication of greater search on global inequality — it is easier to identify resources outside a local area. That should reduce rents and result in more producers (ie workers) receiving the marginal product of their labour as determined by global prices, rather than local prices. In this way, quantum computing drives economic efficiency.

Quantum and the digital stack

Of course other transactions costs (the cost of making the exchange, the cost of contract enforcement etc), can reduce the opportunities for faster search to disrupt existing patterns of economic activity. Here we argue that quantum is particularly effective in an environment of digital (or digitised) trade and production — in the domain of the information economy.

The process of digitisation is the process of creating more economic objects and through the use of distributed ledgers and digital twins, forming more and more precise property rights regimes. In Berg et al (2018), we explored one of the implications of this explosion in objects with precisely defined property rights. We argued that the increasingly precise and security digital property rights over objects would allow artificially intelligent agents to trade assets on behalf of their users, facilitating barter-like exchanges and allowing a greater variety of assets to be used as ‘money’. Key to achieving this goal is deep search across a vast matrix of assets, where the optimal path between two assets has to be calculated according to the pre-defined preferences not only of the agents making the exchange, but of each of the holders of the assets that form the paths.

This illuminates one of the ways in which quantum interacts with the web3 tech stack. While some quantum computation scientists have identified the opportunity for quantum to be used in AI training, we see the opportunity for quantum to be used by AI agents to search for exchange with other AI agents; an exchange theoretic rather than production-centric understanding of quantum’s contribution to the economy. The massive technological change we are experiencing is both cumulative and non-sequential — rapid developments in other parts of the tech stack further drive demand for the quantum compute. This is the digital quantum flywheel effect.

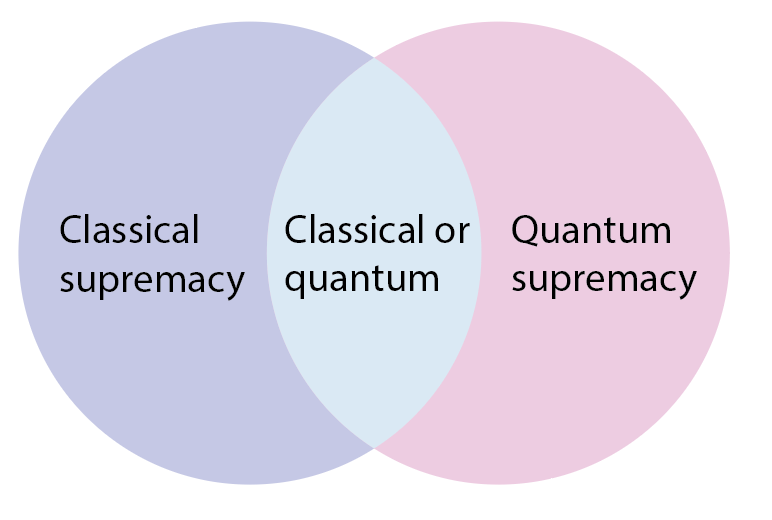

Compute as a commodity

Compute is a commodity and follows the rules of commodity economics. Just as buyers of coal or electricity are ultimately buying the energy embodied in those goods, buyers of compute are ultimately buying a reduction in the time it takes to perform a computational task (Davies 2004). There are computational tasks where classical computers are superior (either cheaper or faster), where quantum computers are superior (or could be superior), and those where both quantum and classical computers can satisfy demand. Users of compute should be indifferent as to the origin of the compute they consume, but they have specific computational needs that they wish to perform subject to budget and time constraints. And they should be indifferent to the mixture of classical and quantum computing that best suits their needs and constraints.

This indifference between classical and quantum has significant consequences for how quantum computing is distributed between firms in the economy — and, indeed, between geopolitical powers. At this stage in the development of quantum computing, the major open question is how relatively large the space of computational tasks that are best suited for classical computing are versus that for quantum computing.

For computational tasks where classical computers dominate, compute is already massively decentralised — not just with multiple large cloud services (AWS, Google etc) but in the devices on our desks and in our pockets. There is no barrier to competition in classical compute, nor any risk of one geopolitical actor dominating. Where bottlenecks in classical compute emerge are in the production networks for semiconductor chips — a known problem with a known menu of policy stances and responses. Similarly, no such risk emerges around computational tasks where classical or quantum systems are equally suited.

The salient question is whether there will arise a natural monopoly in quantum compute? This could arise as a result of bottlenecks (say of scarce minerals, or caused by market structure as in the semiconductor chip industry), or as an outcome of competition in quantum computing development. As an example, one argument might be that as quantum compute power scales exponentially with the number of qubits then a geopolitical or economic actor that establishes a lead in qubit deployment could maintain that lead indefinitely due to compounding effects. This is a quantum takeoff analogous to the hypothesised ‘AI takeoff’ (see Bostrom 2014).

Several factors mitigate against this. The diversity of architectures for quantum computing being built suggests that the future is likely to be highly competitive; not merely between individual quantum compute systems but between classes of architectures (eg. superconducting, ion trap, photonics). While quantum compute research and development is very high cost, it is proceeding widely and with significant geographical dispersion. There are at least eight distinct major systems or architectures for quantum computing, seven of which have successfully performed basic computational tasks such as the control of qubits (see the survey by Bremmer et al 2024).

Nor is there any obvious concern that first-mover advantage implies competitive lock-in. Quantum compute is quite unlike AI safety scenarios, where ‘superintelligence’ or ‘foom’ is hypothesised to lead to a single monopolistic AI as a result of the superintelligence using its capabilities to 1) develop itself exponentially and 2) act to prevent competitors emerging. Quantum computing is and will be, for the long foreseeable future, a highly specialised toolset for particular tasks, not a general program that could pursue world domination either autonomously or under the direction of a bad actor.

One significant caveat to this analysis is that the capabilities of quantum compute might have downstream consequences for the economy, and this could . The exponential capabilities at factoring provided by quantum compute could undermine much of the cryptography that protects global commerce, and underlines the need for the development and deployment of post-quantum cryptography. We have argued elsewhere that the signals for the emergence of quantum supremacy in code breaking will emerge in the market prices of cryptocurrency (Rohde et al 2021). There is a significant risk mitigation task ahead of us to adopt post-quantum cryptography. It is a particularly difficult task because while the danger is concrete, the timeline for a quantum breakthrough is highly uncertain. Nonetheless, the task of migrating between cryptographic standards is akin to many other cybersecurity mitigations that have been performed in the digital economy, and while challenging should not be seen as existential.

Instead, the institutional economic view of quantum computing emphasises the possibilities of this new technology to radically grow the space for market exchange — particularly when we understand the possibility of quantum computing as co-developing alongside distributed ledgers, smart contracts (that is, decentralised digital assets) and artificial intelligence. Quantum computing lowers the cost and increases the performance of economic exchange across an exponentially growing ecosystem of digital property rights. It will be an important source of future economic value from better economic institutions.

References

Berg, Chris, Sinclair Davidson, and Jason Potts. ‘Beyond Money: Cryptocurrencies, Machine-Mediated Transactions and High-Frequency Hyperbarter’, 2018, 8.

Bremner, Michael, Simon Devitt, and Dr Eser Zerenturk. “Quantum Algorithms and Applications.” Office of the NSW Chief Scientist & Engineer, March 2024.

Bova, Francesco, Avi Goldfarb, and Roger G. Melko. ‘Commercial Applications of Quantum Computing’. EPJ Quantum Technology 8, no. 1 (December 2021): 1–13. https://doi.org/10.1140/epjqt/s40507-021-00091-1.

Rohde, Peter P, Vijay Mohan, Sinclair Davidson, Chris Berg, Darcy W. E. Allen, Gavin Brennen, and Jason Potts. “Quantum Crypto-Economics: Blockchain Prediction Markets for the Evolution of Quantum Technology,” 2021, 12.

Roth, Alvin E. ‘The Economics of Matching: Stability and Incentives’. Mathematics of Operations Research 7, no. 4 (1982): 617–28.

Stigler, George J. ‘The Economics of Information’. Journal of Political Economy 69, no. 3 (1961): 213–25.

Abstract: Decentralised Autonomous Organizations (DAOs) are a typical organisation form in the Web3 economy. DAOs are internet-native organisations that are coordinated and governed by pseudonymous community members through a nexus of blockchain-based digital assets and smart contracts. There is over US$26 billion locked in over 2,300 active DAOs globally. This article examines the legal recognition of DAOs in an Australian context. A recent Australian Senate Inquiry recommended DAOs be recognised as a distinct business structure. This article makes three contributions towards this goal: (1) critically evaluate options for DAO recognition under Australian law; (2) a comparative analysis of United States DAO laws; and (3) an analytical outline of the key design features of an Australian DAO law.

Author(s): Aaron M. Lane, Darcy W. E. Allen, Chris Berg

Cite: Lane, Aaron M., Darcy W. E. Allen, and Chris Berg. “Towards Legal Recognition of Decentralised Autonomous Organisations.” Australian Business Law Review, vol. 52, 2024, pp. 96–116.

Abstract: We propose a new theory of stablecoins based on common knowledge. We contrast this with the ‘better money’ theory of stablecoins, which emphasises marginal improvements over the standard origin of money theory as: medium of exchange, unit of account, store of value.

With Julian Waters-Lynch, Darcy WE Allen, and Jason Potts. Available at SSRN.

Abstract: This paper explores the management challenge posed by pervasive and unsupervised use of generative AI (GenAI) applications in firms. Employees are covertly experimenting with these tools to discover and capture value from their use, without the express direction or visibility of organisational leaders or managers. We call this phenomenon shadow user innovation. Our analysis integrates literature on user innovation, general purpose technologies and the evolution of firm capabilities. We define shadow user innovation as employee-led user innovation inside firms that is opaque to management. We explain how this opacity obstructs a firm’s ability to translate the use of GenAI into visible improvements in productivity and profitability, because employees can currently privately capture these benefits. We discuss potential management responses to this challenge, outline a research program, and offer practical guidance for managers.

Abstract: In this paper, we examine the usefulness of time commitment as a voting resource for decentralized governance when the identity of voters cannot be verified. In order to do so, we take a closer look at two issues that confront token-based voting systems used by blockchain communities and organizations: voter fraud through the creation of multiple identities (Sybil attack) and concentration of voting power in the hands of the wealthy (plutocracy). Our contribution is threefold: first, we lay analytical foundations for the formal modeling of the necessary and sufficient conditions for a voting system to be resistant to a Sybil attack; second, we show that tokens as the only instrument for weighting votes cannot simultaneously achieve resistance to both Sybil attacks and a plutocracy in the voting process; and third, we design a voting mechanism, bond voting, that is Sybil resistant and offers a second instrument (time commitment) that is effective for countering plutocracy when large token holders also have a relatively high opportunity cost of locking tokens for a vote. Overall, our paper emphasizes the importance of time-based suffrage in decentralized governance.

Abstract: Interoperability describes the ability of systems to share services and resources with other systems. It is used in many fields — in the law, in communications and payments systems, in healthcare systems and in military alliances, to name a few — and describes a large number of characteristics from technical standards, to information architecture, to organisational governance. This glossary entry presents a topology of interoperability layers and presents some of the key economic and socio-technical concerns faced by interoperable systems.

Abstract: Interchain security (ICS) allows the Cosmos Hub to provide security to other blockchains (‘consumer chains’) and represents a significant revenue model for the Cosmos Hub. This paper investigates the economic and governance aspects of these ICS agreements with a focus on ensuring that the agreements are value adding and robust. The paper identifies potential risks such as vertical integration, challenges in adapting to incomplete contracts, and opportunism in asset-specific investments. It proposes recommendations to enhance the sustainability of ICS relationships, including the establishment of individual governance bodies for each ICS agreement, strategies to manage foreign exchange risks, and a decision tree for the Cosmos Hub to assess new consumer chains. A draft template for consumer chain onboarding is also presented, detailing essential elements like governance, payment terms, and exit clauses. This paper aims to offer actionable insights for improving the governance structures in ICS agreements, thereby fostering robust and enduring interchain security dynamics.

Abstract: This paper helps allocate shared capital effectively in the Cosmos ecosystem by examining a range of different allocation mechanisms. We identify the core challenges of allocating shared capital – with a focus on knowledge, opportunism and coordination problems. We outline four mechanisms that capital allocation DAOs can use to allocate capital in different contexts: grants, prizes, tenders and in-house production. Each have implications for the transparency and accountability of capital allocation. Our findings help capital allocation DAOs make decisions about how to allocate shared capital across the Cosmos ecosystem.