With Sinclair Davidson and Jason Potts. Originally a Medium post.

Satoshi Nakamoto said Bitcoin would be “very attractive to the libertarian viewpoint”. The pioneers of cryptocurrencies were cypherpunks or crypto-anarchists who wanted to use this new invention to escape the state’s monopoly on money.

We’re sympathetic to this — as we argued in our last Medium essay ‘Byzantine Political Economy’.

But the state is not so easy to escape.

Not only are there many blockchain use-cases for government, but it is possible that positive government action could help the blockchain revolution along.

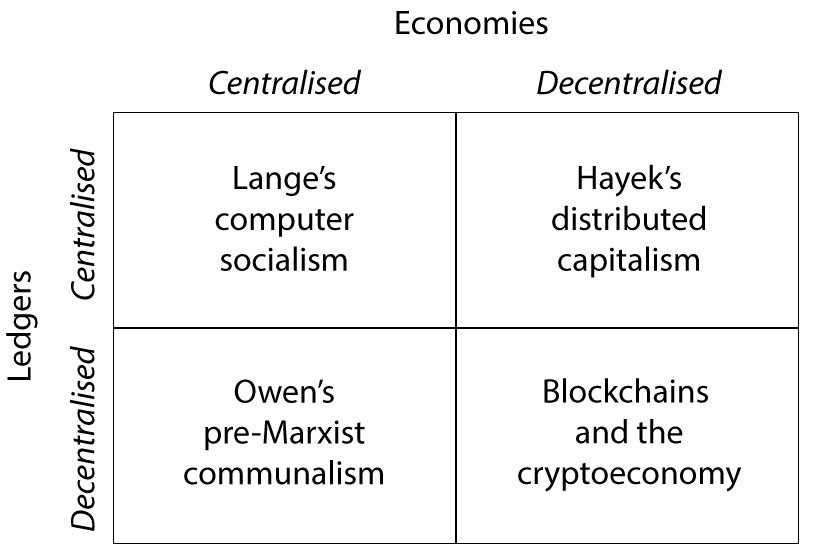

Just as the blockchain radically decentralises economic activity, the born-global nature of the blockchain can radically decentralise economic power.

Crypto-friendly governments — that is, governments that can rapidly adjust their regulatory frameworks to suit the blockchain economy — have a unique window to attract global investment.

Crypto-friendly governments: the state of play

A number of smaller countries and autonomous regions are trying to position themselves as crypto-friendly.

Both Great Britain and Australia have issued high-level government science reports on the prospects of the technology.

Other smaller countries (such as Estonia) and city-states (such as Singapore) have folded blockchain into a digital and e-government investment strategy.

City-states such as Dubai and states or cantons such as Zug in Switzerland and Illinois in the United States are trying to move many aspects of government services to the blockchain, or to create special crypto-economic zones.

Singapore and Australia have directed their financial regulators to issue detailed guidance about the regulatory, legislative and tax treatment of crypto-assets.

Political leaders in Japan and Russia have made multiple announcements broadly supportive of crypto-investment.

Those are the good news stories. However, most countries maintain a sort of benign neglect — either because of the relative small presence of the cryptoeconomy or lack of government interest or capability in the space.

And a small number of jurisdictions are outwardly hostile. New York adopted a hard line in terms of regulatory compliance when it introduced the BitLicense. China has banned initial coin offerings and cryptocurrency exchanges.

Global differences are going to matter

So far, the development of cryptocurrencies has been geographically concentrated in regions like Silicon Valley. But that won’t last. The blockchain is a distributed technology. The relationship between the regions that develop the technology and the regions that adopt the technology is unlikely to be strong.

In other words, the geography of invention is not the same as the geography of innovation.

The United States is highly successful in inventing blockchain technology. Yet it has been finding it hard to adopt blockchains because of American regulatory complexity.

Regulatory agility will be a significant factor determining which nations are able to successfully adopt blockchain technology.

This favors city-states (Singapore), smaller countries (Estonia, Australia) and subnational jurisdictions (Zug, Illinois).

The blockchain tax problem

How should cryptoassets be taxed? Are tokens money (taxed as spending)? Or are they debt or equity (in which case it would be treated as income or gains from a capital asset or investment vehicle)? We’ve argued that they cryptoassets are in fact the hypothetical asset class that Nobel laureate Oliver Williamson once called ‘dequity’. This means they should be taxed as capital assets, not as money.

But blockchain technology is not just another productivity enhancing technology that can be taxed at the point of adoption. Blockchains are actively associated with tax avoidance or tax shifting owing to the pseudonymous nature of transactions and the difficulty of establishing the correct jurisdiction for taxation.

This is going to be hard to unravel. As Chris and Sinclair told an Australian parliamentary inquiry in October 2017, blockchain-enabled organisations

are going to be harder to tax than the monolithic firms of the 20th century. We’ve published sceptically about the parliament’s efforts to prevent profit shifting by multinational firms. However, the born-global nature of blockchains will supercharge these trends. We do not believe there will be any easy regulatory solution to this, and parliament will need to rethink not just how it taxes, but what it taxes.

What should government do?

Nakamoto did not develop Bitcoin in a vacuum.

To the extent that government funding of academic mathematicians and cryptographers produced the initial research papers that were subsequently developed into the blockchain, then the early development of this technology was publicly sponsored — but not publicly planned.

Should government do more on the research side?

Let’s first assume that governments are benevolent — call this the public interest model of government.

Many economists, following Kenneth Arrow’s 1962 paper ‘Economic Welfare and the Allocation of Resources for Invention’, argue that the uncertainties and positive social benefits from invention can lead to a market failure in research and development.

It’s not clear that the blockchain has this problem. This is in part because token sales incentivise early adoption. What some people are calling a ‘bubble’ we think is massive experimental investment.

Alternatively, governments could substitute blockchains for their own existing services like the provision of money or property registries.

Governments should pick specific use-cases — such as identity and asset registries, licenses and certification, open government data, reporting and management of government contracts and public assets — then estimate the marginal cost and benefits of investment and adoption of this technology.

These benefits could be huge. For instance, a Bank of England report estimates a 3 percent gain in GDP from issuing a government cryptocurrency.

Other potential government involvement could focus on public goods problems — such as the need for the network communications infrastructure upon which a cryptoeconomy operates (particularly in the developing world).

Governments could also create open access data regimes and registries that can be harnessed and used by cryptoeconomy businesses.

But most fundamentally, governments should invest in high quality legal institutions (regulators, courts, bureaucracies, democratic systems, etc) to provide the cryptoeconomy with the needed predictability, efficiency, transparency, accountability, and efficacy.

But then again…

Why might some countries fail to make the necessary reforms for the blockchain economy? Governments might not know about the benefits or might misunderstand them (bounded rationality or information constraints). Governments might not be able to afford the necessary public investment (financial constraints).

Or we might not trust government enough. There are huge efficiency gains to be made from moving government registries like identity, property titling, tax, voting, central bank coin to the ‘trustless’ blockchain. But to do so itself requires high levels of trust in the government making that change.

This is the paradox: it takes a lot of trust to get to trustlessness. Sweden and Australia will be able to move easily to distributed land title registries. Haiti (where the need for a distributed land title register is much greater) will find it harder.

Governments against blockchains

Radical decentralisation will not always be in the interest of centralised governments.

In the public choice model of government, both governments and citizens have distinct objectives that they seek to maximize.

Citizens trade votes for services. Governments seek to create benefits for themselves (subject to the constraint of getting elected). What citizens want and what governments conflict, resulting in political exchange.

Take blockchain-enabled identity. From the perspective of the government, each citizen ought to have one and only one identity. A single, centralised identity is useful for entitlements and taxation — or conscription.

These centralised identity registrations are co-opted for commercial uses of identity (e.g. to open a bank account, or to rent a car).

But from the citizen perspective this is inefficient, because as identity is owned and managed by the state, they have no control over it, and cannot choose how to permission and share this data. It also creates problems of trust and privacy (for example in health and criminal records).

A decentralized identity would be more efficient, facilitating variety of types of identity for specialized uses and enabling user control. Citizens might want this. Governments do not.

What will other governments do?

Ideally, the approach of governments to the blockchain economy would be both rationally optimal from the perspective of its own citizens, but also a best response to the expected moves of foreign governments — many of which will differ in size, level of economic development, and institutional quality.

For instance, there is no doubt that many tax bureaucracies would like to constrain or control the growth of the cryptoeconomy as it will make taxation harder.

But their success will depend on what other countries as well.Blockchains — and the wealth and relationships on the blockchain — are both everywhere and nowhere.

In this world, it is not obvious what most effective public policy settings will be. There will be heavy learning costs involved. Some governments might rationally decide to delay decision making in order to learn from first-movers who can then be expected to incur costly mistakes in the experimental process of policy settings.

It is possible that larger countries will be much more cautious in adopting cryptoeconomic policies that are significantly divergent from other competing countries.

Alternatively, we could see bilateral or club-like coalitions of strategic investment and public policy harmonization — just as we do with tax and trade treaties.

Private governance and crypto-secession

When governments are particularly oppressive, blockchains can be used to move many aspects of an economy away from central control (identity, contract, money and payments, organization, data, etc). This allows what Trent MacDonald calls nonterritorial secession, or crypto-secession.

In the classic federal model of local public goods, governments competitively provide public goods with different offerings and price points. If an individual prefers a different bundle of public goods, they move to another jurisdiction. If a group of individuals collectively prefers a different bundle of pubic goods, they secede. But to secede, they have to physically move somewhere else, which is costly.

Non-territorial secession allows individuals to choose a different bundle of public goods without having to move. They just opt out of all or part of the government bundle. Crypto-secession is when the new bundle of local public goods is organized, coordinated and delivered through blockchain technology.

What does this mean in practice? An example of such emergent private governance of local public goods might occur at a local or regional level where a group of citizens create a pooling mechanism of social insurance, energy grid, or asset titling management through smart contracts, decentralised applications and distributed autonomous organisations.

This is more likely at the local, regional or city level than that of a nation state because of set-up costs and self-selection. We expect that the adoption of blockchain technology for governance will be a bottom-up phenomenon beginning with small groups.

Blockchains and property rights

Blockchain technology may also disrupt the relationship between government and property rights.

A fundamental question in the economics of law is this: Do property rights originate from the state and are then used by market participants? Or do property rights arise from markets and economic activity, and are thenefficiently enforced by the state?

While the former view (legal-centrism) is the most widely held among law and government scholars, public choice and market institutional economists tend to defend the latter (evolutionary) view.

Cryptocurrencies and crypto-assets provide a test of these competing views. It is not obvious what role the state plays in either creating or enforcing the property right claims over these assets.

One argument is that cryptocurrencies and crypto-assets have emerged entirely outside state jurisdiction and instead occupy a new software-enforced constitutional governance realm. In this strong form view, these are native crypto-property rights from which there is a risk of government predation.

An alternative argument is superficially similar, but allows that this parallel crypto-property rights regime has emerged in-the-shadow-of state law and enforcement. Crypto-property rights will remain in the domain of private law only until there are irreconcilable disputes, at which point there will be a role for government enforcement and sanctions.

This distinction about the origins of property rights matters because while governments provide public goods and support property rights(emphasised by the legal-centric school), they also impose costs by accumulating power (emphasised by the evolutionary school). A crypto-property rights regime will test which of these is more significant.

Creative destruction

Governments may also find themselves addressing the effects of creative destruction in a blockchain economy.

Past experience has shown that governments often end up supporting or compensating those negatively affected by new technology. They also end up making complementary investments such as education and workforce retraining.

The risk is that without such government action those who expect to be harmed by the adoption of a new technology may form political coalitions to block or raise the costs of developing the new technology.

Blockchain technologies face substantial hurdles from incumbents and vested interests that might lobby to slow or outright ban uses of the technology.

Governments may find themselves on both sides of creative destruction, seeking to promote the adoption of blockchains for social welfare maximizing reasons, while at the same time being captured by vested interests seeking protection.

Blockchain public policy

The blockchain is an extremely new technology. There is substantial uncertainty associated with its future uses, adoption levels — even its basic economic properties.

But it will be disruptive. And despite the libertarian, secessionist ethic of the blockchain community, government will be involved, for better or worse.The goal for the blockchain community and for crypto-friendly governments ought to be ensuring that this technology can be adopted in a way that benefits citizens, not rent-seekers.