Telstra was sold barely a year ago, but both major parties want to bring the government back into the telecommunications infrastructure game.

The Federal Government has responded to its own failure to reform the decade-old regulatory framework for telecommunications with an array of subsidies and initiatives to introduce high-speed broadband networks. In response, the Labor Party dangles in front of voters a $4.7 billion high speed fibre-optic network.

Both parties are trying to make political capital out of the regulatory quagmire which government action has created for the telecommunications industry. But their proposals offer far less than substantive regulatory change could, and they offer it at a much greater cost to taxpayers.

How broadband became an election issue

A decade is a long time in the communications industry.

In 1997, the ABS reported that barely 300,000 Australians subscribed to Internet connections. In 2007, that figure is now six-and-a-half million. (The number of actual users is far higher. With modern networking hardware not widely available a decade ago, many people share Internet access in the household or workplace.)

With the limited speeds offered by dialup technologies, accessing video and audio was then idle futurism. Today, some estimates place video and audio downloads at 90 per cent of traffic.

Nevertheless, the regulatory framework which was developed in 1997 to govern the industry remains the same regulatory framework governing the industry in 2007. While technology and consumption patterns are almost unrecognisable a decade later, the regulation hasn’t budged.

This regulatory framework was designed to encourage the competitive provision of telecommunications using the legacy infrastructure owned by Telstra. By purchasing capacity from the infrastructure owner, competitors could share the network, introducing competition where previously there was none, and without the need for competitors to build their own network from scratch. The approach favoured by regulators under such a framework is to encourage competitors first to resell Telstra’s products, and then progressively to install hardware into the network to compete with the dominant telco.

With carefully regulated access prices, this ‘ladder of investment’ is designed to encourage both competitors and incumbents to invest in infrastructure—the former in order to siphon off some of the market share of the incumbent; the latter to invest to stave off hungry competitors.

The high level of competition for basic internet and telephony service attests to the success — at least on one metric — of this regulatory model. Indeed, at one time, there were more than 600 internet service providers (ISPs) in Australia.

But a mere two dozen of those have had more than 10,000 customers, and competition is not merely a synonym for ‘lots of companies’. Most Australian ISPs are small shoestring operations — reliant on regulated access prices for reselling Telstra services, and highly prone to failure. This segment of the industry looks like a caricature of the economic models of ‘perfect competition’ — hundreds of companies, prices down to marginal cost, and homogenous products.

Nevertheless, the structure of the market is not the most significant flaw in the existing regulatory framework. Critically, the ‘ladder of investment’ theory is unable to deal with major shifts in technology. When it becomes time to move beyond the legacy copper-wire network — the need for a fibre-optic network in Australia is manifestly clear — access regulations are unable to encour-age the creatively destructive investments required.

After all, regulators have encouraged firms to invest further and further into the existing Telstra infrastructure. These firms rely on a specific regulatory framework to provide them with a business model. Furthermore, the prospect of entirely new networks threatens their existing hardware investments — a fibre-optic network may strand a firm’s assets, or at the very least provide unwelcome competitive pressures. Understandably, these firms resist any proposed change to the telecommunications access regime.

The ‘ladder of investment’ may encourage investment up the ladder, but it discourages investment in alternative ladders. There have been indications that this framework was distorting investment for some time. Optus had been migrating customers off its own cable network and on to the Telstra network when the regulated access price turned in its favour. Fearful of having its service declared by regulators as open access, Telstra is only turning on its recently upgraded high-speed ADSL2+ equipment in areas where there is investment from competitors — in Tasmania, for example, the telco has installed ADSL2+ in more than 100 telephone exchanges, but has switched it on in only three.

But the big evidence came in a flurry of controversy last year. The impasse between the Australian Competition and Consumer Commission (ACCC) and Telstra late last year over the access price for their proposed fibre-to-the-node network pivoted around the application of the regulatory framework to new infrastructure investments.

The fact that the two organisations could not come to an agreement (Telstra very publicly announced that it was scrapping its plans to build a new network) should have provided federal policymakers with a very clear indication that the decade-old regulations had finally collapsed.Unfortunately for taxpayers, this was not to be the case. Instead of reform, the political reaction to this regulatory failure has been to propose subsidies, grants, programmes, initiatives and plans. Worse — all of the proposals on the table would increase government involvement in communications investment, not decrease it.

With the ink barely dry on the full sale of Telstra, das broadband problem has politicians wanting to try their hand again at managing the telecommunications industry.

Picking winners, 2007 style

When Communications Minister Helen Coonan announced a one billion dollar award to an Optus–Elders consortium (dubbed ‘Opel’) to deploy a WiMAX wireless network for regional and rural broadband, she had to defend the technology against its legion of critics.

WiMAX is a successor technology to the WiFi standard that is common in home internet networks. In optimal conditions — that is, with access to the right licensed spectrum band, and in the best geographic and environmental circumstances—the technology can deliver broadband speeds at distances of up to ten or fifteen kilometres, wirelessly from the base station.

However, WiMAX’s reputation has suffered from over-hype. Early enthusiasts proclaimed a range of seventy kilometres, and when the technology failed to deliver even half of that, cynicism about its capabilities crept in.

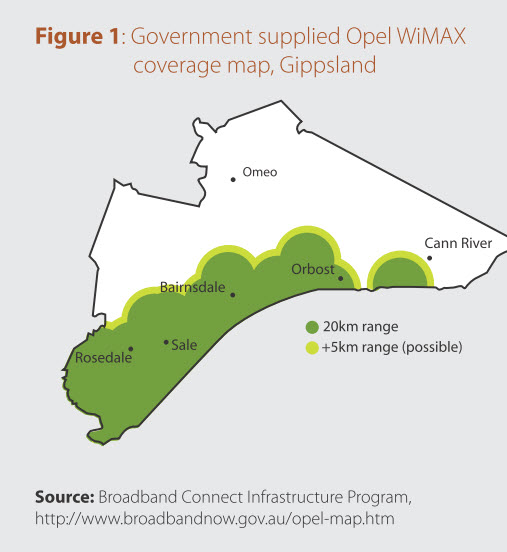

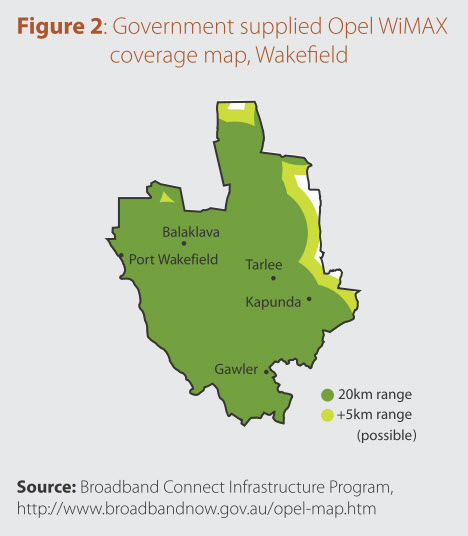

The Communications Minister has not avoided this trap. Releasing maps of the coverage of the Opel network, the Government has assumed a range of 20 kilometres, with a ‘possible’ further 5 kilometres, a much further distance than the broadband is likely to be available.

Two other factors work against the network’s favour. First, the Opel network will deploy a ‘fixed’ WiMAX network, which is being superseded by the superior ‘mobile’ WiMAX technology. Second, such range is only possible on licensed spectrum, to which the Opel network does not currently have access. WiMAX operating on unlicensed spectrum has to compete with a range of consumer technologies such as home wireless phones, private radio transmitters, garage door openers, and so on.

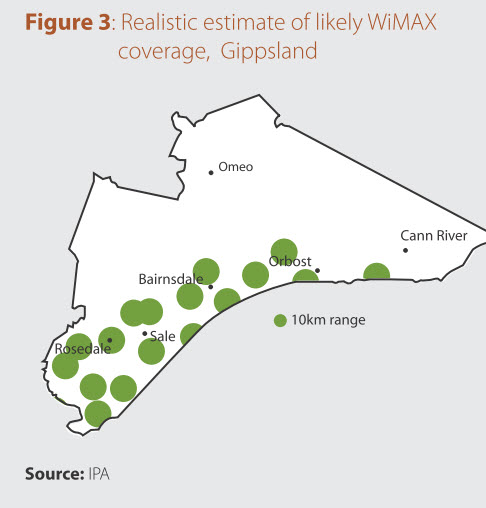

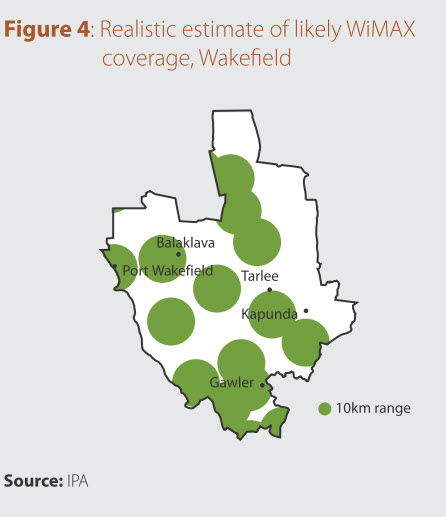

Given these problems, a more likely range for the WiMAX deployments would be in the region of five to ten kilometres. To be uncharitable, when considering environmental and topographical factors, a maximum range of as little as one or two kilometres is entirely possible.

When the maps of WiMAX coverage that were paraded around by the Communications Minister after the Opel announcement are redrawn with a more realistic range, the difference is stark.

Figures 1 to 4 illustrate this difference in two marginal electorates — Gippsland in rural Victoria, and Wakefield in northern Adelaide. (In an election year, electorates are always the most appropriate unit of measurement.) Figures 1 and 2 are the maps produced by the Department of Communications, which assume a twenty kilometre range with a possible added 5 kilometres for the WiMAX network. Figures 3 and 4 depict what the coverage would be like when we assume a more realistic, but still charitable, range of ten kilometres. In both cases, what appeared to be blanket coverage is now revealed as relatively spartan.

A range of ten kilometres may still be too optimistic. Many WiMAX experts predict even less—down to five, or even one or two kilometres. Experience with a similar technology used by the wireless ISP Unwired in Sydney gives little hope. That the likely range of a wireless network could be overestimated is certainly not unique. A firm competing in an open market that found its network was under performing would merely deploy more towers or upgrade to a better technology. But when the source of funding is public dollars, it should be of some concern.

As these maps make clear, it is highly unlikely that the one billion dollar grant for rural broadband will produce the services advertised.

There is one further core problem with the Federal Government’s rural broadband proposal. While the choice of WiMAX has been the major public focus, the Opel plan also relies on widespread ADSL2+ installations. (For instance, Omeo in Gippsland will be serviced by ADSL2+, rather than WiMAX.) However, as we have seen above, Telstra has deployed ADSL2+ in hundreds of exchanges, but because of the risk of regulatory appropriation, has not switched it on until there has been competing investment.

It is yet another striking demon-stration of the perversity of the regulatory framework that governs the sector: once Opel has installed its equipment in exchanges around the country, and as a result Telstra feels free to switch its equipment on, taxpayers will have paid to build duplicated infrastructure.

Broadband to urban areas is to be dealt with separately, and a taskforce set up by the Government has released guidelines for firms applying to build a network. Applicants have until April to apply, and can specify any necessary regulatory changes required. The minister has gone so far as to suggest that one possible regulatory change would be to grant an infrastructure monopoly to the successful firm to protect it from competition, something which would resemble the legislative monopolies that have characterised Australia’s economic history for most of the twentieth century. Nevertheless, one of the core guidelines recommended by the taskforce is the maintenance of an ‘open access’ regime.

It is clear that few lessons have been drawn from the failures of access regulation in the telecommunications sector.

‘Well, we could just pay for the damn thing ourselves’

While the federal government has provided the most detailed plans, they were beaten to the punch by the ALP. In March, the Federal Labor Party announced its solution to the broadband problem — a $4.7 billion grant to build a national fibre-optic broadband network. Specifically, the ALP proposes a fibre-to-the-node network, which is the same sort of network that Telstra proposed and then abandoned six months earlier.

There is a degree of irony when con-sidering the source of the $4.7 billion. $2.7 billion will come out of existing communications funds—a legacy of the more than a dozen broadband infrastructure programmes of the Howard Government’s last five years. But the remaining two billion dollars will be drawn from the Future Fund, itself a result of the sale of Telstra. Telstra is, as the country’s biggest telecommunications infrastructure providers, likely to be a big contender for the grant. The ALP proposal may return to Telstra the proceeds of its own sale.

But less facetiously, it is hard to justify the use of taxpayer money to build a network that the private sector — in this case, Telstra — was desperate to build itself. And instead of regulatory reform, both the ALP proposal and the Federal Government’s proposal lock the telecommunications sector back into a cycle of government investment and regulated access.

To appropriate the graceless expression made famous by the Communications Minister, neither proposal adequately ‘future-proofs’ the communications sector. When the next inevitable infrastructure upgrade is faced — fibre-to-the-node is hardly the last communications network that will be built in Australia — the same regulatory challenges will arise, unless a more comprehensive and ‘future’ orientated reform is pursued.

As Alan Moran and Warren Pengilley have demonstrated in their recent Institute of Public Affairs monograph, Regulation of Infrastructure: Its Development and Consequences, telecommunications is hardly alone in suffering from inappropriate access regulation. Ports, gas, airports, electricity and railroads have all been negatively affected by infrastructure regulation which grants competitors access to their networks at a regulated price.

In telecommunications, a regulatory framework that includes a disincentive to invest is particularly damaging — technological change requires continuous investment. Broadband in Australia is less than it could be, not because the federal government has failed to assume responsibility for its infrastructure, but because it refuses to reform obsolete regulations that hold private investment back. Bringing the government back into the telecommunications market is no solution.