Abstract: Ronald Coase famously argued that “if an economist finds something – a business practice of one sort or other – that he does not understand, he looks for a monopoly explanation”. So it is with credit card interchange fees. Intellectual confusion has led to the phenomenon of interchange fees being misdiagnosed as being a monopoly problem leading to inappropriate policy intervention. Following George Stigler’s path breaking analysis of the US Security and Exchange Commission he claimed that financial regulation was “founded upon prejudice and … reforms are directed by wishfulness”. In our opinion, Australian regulatory attitudes towards interchange fees should be placed into the same category: reforms initiated by ignorance and anti-bank prejudice.

As goods move between firms and across borders, information about the provenance, characteristics, and compliance liabilities (whether they are subject to taxes or tariffs) of those goods move alongside them.

Handling companies need to know which goods are going where.

Regulators and trade authorities need to know whether the goods crossing a national border are compliant with domestic regulations.

(Does a good need an import permit? Does it require any special documentation? In Australia the Minimum documentary and import declaration requirements policy is a 27 page document.)

And end-users increasingly demand information about where their goods came from and how they were produced.

(Consumers want to know where their food is grown, whether it was grown to organic standards, or was manufactured gluten-free or nut-free. Advanced manufacturing firms want assurances that components — such as aircraft or wind turbine parts — are of high quality. And everyone wants assurances that their goods have been looked after while in transit.)

The result is piles of documentation shipped alongside internationally traded goods.

And the demand for documentation is growing. Supply chains are getting more complex. Regulatory requirements are increasing. End-users want more information about what they’re buying.

Introducing TradeTech

FinTech is the application of new technology — particularly developments in computer science — to the financial services industry. RegTech does the same for regulatory compliance.

Now we have TradeTech — the application of information technology to reduce the information costs of international trade.

TradeTech can reduce transaction costs, increase transparency for firms, regulators, and consumers, facilitate trade finance, and significantly lower regulatory and tariff compliance burdens.

Tackling border costs

One TradeTech application, blockchains used to manage supply chains, have the potential to provide a new digital services infrastructure for international trade in goods.

Blockchains can store information about the provenance and distribution of tradable goods through the entire supply chain in circumstances where firms (and regulators) through the supply chain do not necessarily trust each other.

The invention of the shipping container in the 1950s radically transformed international trade by tackling the high cost — and unreliability — of getting goods on and off ships intact.

But in the 2010s, it isn’t the cost of transport that is the biggest burden on international trade. According to IBM and Maersk, the costs of bringing goods across borders are higher than the costs of transport costs.

In 2018 and 2019 we expect blockchains used in supply chains and to facilitate global trade will be one of the breakthrough blockchain use cases.

The impact of this sort of TradeTech will provide an enormous boost to the potential for global trade.

Facilitating trade flows

The information flows that facilitiate international trade are still to a remarkable degree governed and organised on a one-to-one basis and using paper. Each firm in a global supply chain passes off information relating to a tradeable good to each other one step at a time, vouchsafing that information until it can be passed to the next firm on the chain.

Furthermore, despite two decades of the digitisation of global commerce, it is still the case that international trade is a significantly paper-based process — which is slow, error-prone and raises fraud risks.

The growth of the regulatory state over the last thirty years has significantly increased the compliance costs of trade. While regulatory harmonisation and tariff reductions have encouraged larger volumes of trade, these have been matched by greater demands for information those goods travelling across borders.

New regulatory concerns about labour, environmental, chemical, and biosecurity standards are being reflected in international trade agreements and are translating into more regulatory requirements at the border.

Longer and more complex supply chains as a result of globalisation has multiplied these compliance burdens.

Blockchains can provide a ‘rail’ on which all this information travels.

Blockchains are uniquely suited for an era of advanced globalisation, the regulatory state, and demand for information about product origins and quality.

But TradeTech needs multilateral coordination

Private industry is developing the technology for blockchain-enhanced supply chains.

But there is the need for an international coordination to ensure that industry is able to exploit the opportunities this technology presents.

For example:information rmanaged on blockchains needs to be accepted as valid and compliant by domestic regulators.

One risk is that industry-developed blockchains might not be not treated as compliant with existing regulations. Goods could then remain subject to existing paper-based processes, necessitating double-handling of compliance and reducing the benefits of blockchain-enhanced trade.

Another risk is that individual trading countries adopt their own standards, which would also necessitate double-handling.

A further risk is that standards are developed by early market leaders in the blockchain-facilitated trade space, are adopted by regulators and trade authorities on an ad-hoc basis, and through regulatory lock-in limit the contestability of this trade infrastructure.

The benefits of TradeTech will be realised in a world of open-standards, rather than closed ones.

Multilateral bodies like APEC (Asia-Pacific Economic Cooperation) should be considering these questions now.

We don’t think governments should try to regulate the development of blockchain technology, or compel its introduction. The blockchain is an experimental technology that needs space to evolve. But there is a clear role for multilateral bodies to set standards for information managed through blockchains.

TradeTech doesn’t need government regulation or direction. But it does need government cooperation.

Abstract: Distributed ledger technology emerged in 2009 as the protocol behind bitcoin, a cryptocurrency with origins in the ‘cypherpunk’ community who sought to use cryptography to secede from government control of money. Bitcoin’s pseudonymous inventor, Satoshi Nakamoto said Bitcoin would be “very attractive to the libertarian viewpoint” and many in the crypto-anarchist community saw, and still see, cryptocurrencies as a means to free citizens from the monetary depredations of governments. But from these revolutionary secessionist origins, it has become apparent that not only are there many possible use cases of distributed ledger technology for government, but that government action through both regulation, legislation, and public investment might be a key factor in the adoption and development of this technological innovation. Governments can use blockchain technology to exploit the service efficiencies they may bring. But also, and perhaps counter-intuitively given their revolutionary origins, blockchain applications are likely to need government cooperation to facilitate adoption and the development of the blockchain economic system.

But now Kodak is exploiting one of the most interesting characteristics of the blockchain (the technology behind Bitcoin) to reshape how we understand and manage intellectual property.

Just like Bitcoin demonstrated it was possible to have a digital currency that didn’t require third parties (banks or governments) to validate transactions, KodakOne hints at a future where intellectual property works without the need for third parties to enforce property rights.

Blockchains are a system of decentralised, distributed ledgers (think of a spreadsheet or database that is held on a number of computers at once). Transactions are verified and then encrypted by the system itself.

Kodak’s plan is to use the Ethereum blockchain to build a digital rights management platform for photographs. Photographers will register their photos on the KodakOne platform and buyers will purchase rights using the KodakCoin cryptocurrency.

The platform will provide cryptographic proof of ownership and monitor the web for infringement, offering an easy payment system for infringers to legitimise their use of photographs.

In one sense, KodakOne resembles one of the many supply chain (or “provenance”) applications for blockchain, which track goods and their inputs (think agricultural products or airplane parts).

But photographs are purely digital assets. In a sense, what we’re seeing is a new form of intellectual property.

In KodakCoin, the underlying asset – the thing that is being bought and sold, the thing that has the economic value – is no longer the photograph, per se. Rather, it’s the entry on the global blockchain ledger. Control of that entry constitutes ownership of the asset.

KodakOne only really gets halfway to this idea. Like so many blockchain applications, the question is how this elegant system will interact with the messy real world. It’s one thing to detect infringing uses of a photograph, it’s quite another to enforce terrestrial copyright law on unco-operative infringers. And KodakOne is hardly the only firm working on digital asset management on a blockchain.

A new kind of intellectual property

But there’s another, more pure example of what blockchains can do for intellectual property that is worth discussing – CryptoKitties.

CryptoKitties is a silly little blockchain game, but the economics are worth taking seriously. Players buy digital cats – cryptographically secure, decentralised, censor-proof digital cats – and breed them with each other. Each cat has a mix of rare and common attributes and the goal is to breed cats with the rarest, most-in-demand attributes.

That’s the game. But in fact what CryptoKitties has invented is a new form of intellectual property. Each cat is a completely unique, entirely digital good. And it is completely, cryptographically secure. It can’t be copied.

Usually the protection of intellectual property requires lawyers and courts. But with CryptoKitties, the intellectual property protection is part of the asset itself – it’s baked in.

This is what blockchains were invented to do. Before blockchains, digital goods could be easily duplicated. That’s a great feature – unless you want to create digital money. Digital money won’t work if everybody can just copy their money and spend it over and over again.

The creator of Bitcoin, known as Satoshi Nakamoto, solved this problemwith Bitcoin’s blockchain. Previous attempts to solve the double-spending problem had relied on trusted third parties like banks to validate transactions. Nakamoto managed to get the network to validate itself.

KodakOne (and CryptoKitties) show us that intellectual property has much the same problem as digital currency – and may have the same solution. There’s no need for trusted third parties (governments) to enforce property rights. The blockchain does that for us.

Of course, there’s a lot of work to be done before we see real benefits from this sort of blockchain-enhanced intellectual property. CryptoKitties is its own new form of intellectual property – but can we retrofit “traditional” cultural goods like photographs, music and movies onto the blockchain?

Digitisation has challenged the protection of intellectual property like never before. Cultural producers need to find some way to be paid for their work. This is the direction we should be looking.

Abstract: Blockchains are the distributed, decentralised ledger technology underlying Bitcoin and other cryptocurrencies. We apply Oliver Williamson’s transactions cost analysis to the blockchain consensus mechanism. Blockchains reduce the costs of opportunism but are not “trustless”. We show that blockchains are trust machines. Blockchains are platforms for three-sided bargaining that convert energy-intensive computation into economically-valuable trust.

Abstract: Identification forms a key part of all but the least sophisticated economic and political transactions. More complex or significant transactions demand more formal identification of the parties involved. In this paper we develop an institutional economics of identity. We distinguish between a Demsetzian evolutionary view of identity institutions and a ‘legal-centric’ view of identity institutions. In the former view, identity is a contextual, fluid and subjective, and evolved for market, social and political exchange. In the latter, identity is uniform and permanent, and created (imposed) by governments. Governments have an interest in identity insofar as identity is used in the process of tax collection, entitlements, and conscription. Private organisations free ride off state-provided identification services. The paper concludes with a discussion about technological change and identity management. We characterise two possible futures: one in which new technologies enable states to create more comprehensive uniform identities, and one in which new technologies enable identities to be ‘federated’ and transferred to citizens.

Satoshi Nakamoto said Bitcoin would be “very attractive to the libertarian viewpoint”. The pioneers of cryptocurrencies were cypherpunks or crypto-anarchists who wanted to use this new invention to escape the state’s monopoly on money.

Not only are there many blockchain use-cases for government, but it is possible that positive government action could help the blockchain revolution along.

Just as the blockchain radically decentralises economic activity, the born-global nature of the blockchain can radically decentralise economic power.

Crypto-friendly governments — that is, governments that can rapidly adjust their regulatory frameworks to suit the blockchain economy — have a unique window to attract global investment.

Crypto-friendly governments: the state of play

A number of smaller countries and autonomous regions are trying to position themselves as crypto-friendly.

Both Great Britain and Australia have issued high-level government science reports on the prospects of the technology.

Other smaller countries (such as Estonia) and city-states (such as Singapore) have folded blockchain into a digital and e-government investment strategy.

City-states such as Dubai and states or cantons such as Zug in Switzerland and Illinois in the United States are trying to move many aspects of government services to the blockchain, or to create special crypto-economic zones.

Singapore and Australia have directed their financial regulators to issue detailed guidance about the regulatory, legislative and tax treatment of crypto-assets.

Political leaders in Japan and Russia have made multiple announcements broadly supportive of crypto-investment.

Those are the good news stories. However, most countries maintain a sort of benign neglect — either because of the relative small presence of the cryptoeconomy or lack of government interest or capability in the space.

And a small number of jurisdictions are outwardly hostile. New York adopted a hard line in terms of regulatory compliance when it introduced the BitLicense. China has banned initial coin offerings and cryptocurrency exchanges.

Global differences are going to matter

So far, the development of cryptocurrencies has been geographically concentrated in regions like Silicon Valley. But that won’t last. The blockchain is a distributed technology. The relationship between the regions that develop the technology and the regions that adopt the technology is unlikely to be strong.

In other words, the geography of invention is not the same as the geography of innovation.

The United States is highly successful in inventing blockchain technology. Yet it has been finding it hard to adopt blockchains because of American regulatory complexity.

Regulatory agility will be a significant factor determining which nations are able to successfully adopt blockchain technology.

This favors city-states (Singapore), smaller countries (Estonia, Australia) and subnational jurisdictions (Zug, Illinois).

The blockchain tax problem

How should cryptoassets be taxed? Are tokens money (taxed as spending)? Or are they debt or equity (in which case it would be treated as income or gains from a capital asset or investment vehicle)? We’ve argued that they cryptoassets are in fact the hypothetical asset class that Nobel laureate Oliver Williamson once called ‘dequity’. This means they should be taxed as capital assets, not as money.

But blockchain technology is not just another productivity enhancing technology that can be taxed at the point of adoption. Blockchains are actively associated with tax avoidance or tax shifting owing to the pseudonymous nature of transactions and the difficulty of establishing the correct jurisdiction for taxation.

are going to be harder to tax than the monolithic firms of the 20th century. We’ve published sceptically about the parliament’s efforts to prevent profit shifting by multinational firms. However, the born-global nature of blockchains will supercharge these trends. We do not believe there will be any easy regulatory solution to this, and parliament will need to rethink not just how it taxes, but what it taxes.

It’s not clear that the blockchain has this problem. This is in part because token sales incentivise early adoption. What some people are calling a ‘bubble’ we think is massive experimental investment.

Alternatively, governments could substitute blockchains for their own existing services like the provision of money or property registries.

Governments should pick specific use-cases — such as identity and asset registries, licenses and certification, open government data, reporting and management of government contracts and public assets — then estimate the marginal cost and benefits of investment and adoption of this technology.

These benefits could be huge. For instance, a Bank of England report estimates a 3 percent gain in GDP from issuing a government cryptocurrency.

Other potential government involvement could focus on public goods problems — such as the need for the network communications infrastructure upon which a cryptoeconomy operates (particularly in the developing world).

Governments could also create open access data regimes and registries that can be harnessed and used by cryptoeconomy businesses.

But most fundamentally, governments should invest in high quality legal institutions (regulators, courts, bureaucracies, democratic systems, etc) to provide the cryptoeconomy with the needed predictability, efficiency, transparency, accountability, and efficacy.

But then again…

Why might some countries fail to make the necessary reforms for the blockchain economy? Governments might not know about the benefits or might misunderstand them (bounded rationality or information constraints). Governments might not be able to afford the necessary public investment (financial constraints).

Or we might not trust government enough. There are huge efficiency gains to be made from moving government registries like identity, property titling, tax, voting, central bank coin to the ‘trustless’ blockchain. But to do so itself requires high levels of trust in the government making that change.

This is the paradox: it takes a lot of trust to get to trustlessness. Sweden and Australia will be able to move easily to distributed land title registries. Haiti (where the need for a distributed land title register is much greater) will find it harder.

Governments against blockchains

Radical decentralisation will not always be in the interest of centralised governments.

In the public choice model of government, both governments and citizens have distinct objectives that they seek to maximize.

Citizens trade votes for services. Governments seek to create benefits for themselves (subject to the constraint of getting elected). What citizens want and what governments conflict, resulting in political exchange.

Take blockchain-enabled identity. From the perspective of the government, each citizen ought to have one and only one identity. A single, centralised identity is useful for entitlements and taxation — or conscription.

These centralised identity registrations are co-opted for commercial uses of identity (e.g. to open a bank account, or to rent a car).

But from the citizen perspective this is inefficient, because as identity is owned and managed by the state, they have no control over it, and cannot choose how to permission and share this data. It also creates problems of trust and privacy (for example in health and criminal records).

A decentralized identity would be more efficient, facilitating variety of types of identity for specialized uses and enabling user control. Citizens might want this. Governments do not.

What will other governments do?

Ideally, the approach of governments to the blockchain economy would be both rationally optimal from the perspective of its own citizens, but also a best response to the expected moves of foreign governments — many of which will differ in size, level of economic development, and institutional quality.

For instance, there is no doubt that many tax bureaucracies would like to constrain or control the growth of the cryptoeconomy as it will make taxation harder.

But their success will depend on what other countries as well.Blockchains — and the wealth and relationships on the blockchain — are both everywhere and nowhere.

In this world, it is not obvious what most effective public policy settings will be. There will be heavy learning costs involved. Some governments might rationally decide to delay decision making in order to learn from first-movers who can then be expected to incur costly mistakes in the experimental process of policy settings.

It is possible that larger countries will be much more cautious in adopting cryptoeconomic policies that are significantly divergent from other competing countries.

In the classic federal model of local public goods, governments competitively provide public goods with different offerings and price points. If an individual prefers a different bundle of public goods, they move to another jurisdiction. If a group of individuals collectively prefers a different bundle of pubic goods, they secede. But to secede, they have to physically move somewhere else, which is costly.

Non-territorial secession allows individuals to choose a different bundle of public goods without having to move. They just opt out of all or part of the government bundle. Crypto-secession is when the new bundle of local public goods is organized, coordinated and delivered through blockchain technology.

What does this mean in practice? An example of such emergent private governance of local public goods might occur at a local or regional level where a group of citizens create a pooling mechanism of social insurance, energy grid, or asset titling management through smart contracts, decentralised applications and distributed autonomous organisations.

This is more likely at the local, regional or city level than that of a nation state because of set-up costs and self-selection. We expect that the adoption of blockchain technology for governance will be a bottom-up phenomenon beginning with small groups.

Blockchains and property rights

Blockchain technology may also disrupt the relationship between government and property rights.

A fundamental question in the economics of law is this: Do property rights originate from the state and are then used by market participants? Or do property rights arise from markets and economic activity, and are thenefficiently enforced by the state?

While the former view (legal-centrism) is the most widely held among law and government scholars, public choice and market institutional economists tend to defend the latter (evolutionary) view.

Cryptocurrencies and crypto-assets provide a test of these competing views. It is not obvious what role the state plays in either creating or enforcing the property right claims over these assets.

One argument is that cryptocurrencies and crypto-assets have emerged entirely outside state jurisdiction and instead occupy a new software-enforced constitutional governance realm. In this strong form view, these are native crypto-property rights from which there is a risk of government predation.

An alternative argument is superficially similar, but allows that this parallel crypto-property rights regime has emerged in-the-shadow-of state law and enforcement. Crypto-property rights will remain in the domain of private law only until there are irreconcilable disputes, at which point there will be a role for government enforcement and sanctions.

This distinction about the origins of property rights matters because while governments provide public goods and support property rights(emphasised by the legal-centric school), they also impose costs by accumulating power (emphasised by the evolutionary school). A crypto-property rights regime will test which of these is more significant.

Creative destruction

Governments may also find themselves addressing the effects of creative destruction in a blockchain economy.

Past experience has shown that governments often end up supporting or compensating those negatively affected by new technology. They also end up making complementary investments such as education and workforce retraining.

The risk is that without such government action those who expect to be harmed by the adoption of a new technology may form political coalitions to block or raise the costs of developing the new technology.

Blockchain technologies face substantial hurdles from incumbents and vested interests that might lobby to slow or outright ban uses of the technology.

Governments may find themselves on both sides of creative destruction, seeking to promote the adoption of blockchains for social welfare maximizing reasons, while at the same time being captured by vested interests seeking protection.

Blockchain public policy

The blockchain is an extremely new technology. There is substantial uncertainty associated with its future uses, adoption levels — even its basic economic properties.

But it will be disruptive. And despite the libertarian, secessionist ethic of the blockchain community, government will be involved, for better or worse.The goal for the blockchain community and for crypto-friendly governments ought to be ensuring that this technology can be adopted in a way that benefits citizens, not rent-seekers.

With Sinclair Davidson. Published in the Journal of Behavioral Economics for Policy (2017), Vol. 1, special issue, pp. 50-52.

Abstract: In this paper we provide a critique of behavioural economics or nudging as a basis for practical policy making purposes. While behavioural economics operates as a plausible critique of standard neoclassical economics, it suffers from the same methodological errors inherent within that tradition. Just as socialist planners lacked the information (and incentives) to allocate resources across an entire economy and economists lack the information to optimally correct externalities, so too libertarian paternalists lack the information to second guess consumer preferences and opportunity costs.

For more than three decades economists and cryptographers have been working on the same problem.

Neither species has recognised their own work in the other.

But it turns out that the question of how to coordinate a society and how to ensure communication can be trusted is the same question differently phrased.

Our argument in this essay is simple: What cryptographers call byzantine fault tolerance and economists call robust political economy is the same thing.

This observation turns out to have some significant consequences for understanding the history of economic thought and the directions of institutional cryptoeconomics.

But to explain why, let’s quickly revisit one of the most important debates in the history of economics.

The socialist calculation debate

Economists from Adam Smith on have sought to explain the wealth of nations — why some nations are prosperous and others are not. By the twentieth century this debate had coalesced into a debate about which of two economic systems (communist central planning or capitalist decentralised markets) were more likely to bring prosperity.

Smith argued that market societies were characterised by spontaneous orders. Social order came from market incentives.

Karl Marx objected that the state (or some central coordinating authority) could produce superior outcomes to the market through conscious, deliberate planning.

Before the socialist calculation debate the liberal critique of socialism focused on the problem of incentives — how could a socialist community convince people to work hard if the product from their labour was redistributed? (See, for example, the discussion of socialism in Bruce Smith’s 1887 book Liberty and Liberalism.)

In 1920 the Austrian economist Ludwig von Mises published Economic Calculation in the Socialist Commonwealth. In this essay, Mises made a new, fundamental critique of socialist planning — the problem of information.

In a market economy, Mises argued, prices constitute signals about the highest value use of a good or service, providing a guide for what goods were in demand, and which were in a glut.

How would [a socialist planner] decide whether to send rubber to Tyre Factory 12 or Hose Factory 7? In a market economy, the factory that needed the rubber most would be willing to pay the highest price. But there is no natural price system in socialism — consumer prices are decided by the planner, and rubber allocated according to their diktat.

Mises’ critique of socialism was extended and elaborated by Lionel Robbins and Friedrich Hayek. Hayek turned this argument into one of the greatest essays in economics: ‘The Use of Knowledge in Society’, where he described prices as a decentralised knowledge network.

Centralised computer socialism

The Mises and Hayek argument today is well known, particularly after they seemed to be proven right by the fall of the Berlin Wall. By contrast, their opponents in the debate are less read today.

Mises and Hayek’s criticism was answered by the Polish economist Oskar Lange and extended by Hayek’s Russian-born student Abba Lerner.

Lange and Lerner accepted the importance of the price system in organising economic activity. But they argued that this system could be simulated mathematically.

Working firmly in the equilibrium economics school Vilfredo Pareto and Léon Walras, they imagined the price system as computational machine. In On the Economic Theory of Socialism, published first in 1936 and 1937, Lange concluded that a socialist economy could simulate the effect of the price system by trial and error.

Lange revisited his argument 30 years later. “Were I to rewrite my essay today my task would be much simpler”, wrote Lange:

My answer to Hayek and Robbins would be: so what’s the trouble? Let us put the simultaneous equations on an electronic computer and we shall obtain the solution in less than a second. The market process with its cumbersome tâtonnements appears old-fashioned. Indeed, it may be considered as a computing device of the pre-electronic age.

Not only could computers simulate the market but the computer could conduct long range planning and implement that plan — “a function which the market never was able to perform”.

How decentralised is Hayek’s market, really?

It is typical to cast these two visions of the economy as Lange’s centralised planned economy and Hayek’s decentralised market.

But Hayekian decentralisation still has a lot of centralisation in it.

Here the Marxists are right. Free markets have an awful lot of state involvement in them. Property is private but its enforcement relies heavily on public authorities — the legal system courts, sheriffs, police.

But what both the Hayekians and the Marxists missed is that property rights are not only about enforcement. They’re about the identification and verification of property rights. And (right now) the state does most of that.

As we argued in our previous essay,so much of what the modern state does is endorse, manage, and verify ledgers of social relations. The state manages the property titles register. It manages ledgers of social security entitlements. It manages the ledgers of who is a citizen and who can therefore participate in political bargaining.

This is a very big, important, and largely unappreciated function that the state fulfills. The state does is in charge of these crucial ledgers because it is a large ‘trusted’ entity. But of course how much we can trust the state is questionable.

The invention of the blockchain presents us with new institutional choices.

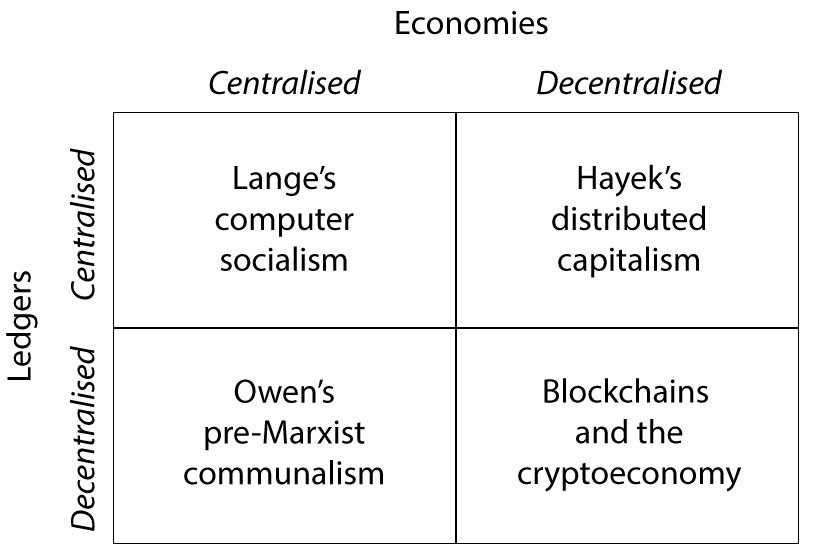

A new typology of political economy

In our new typology of political economy, political ideas are arranged in a grid of centralised and decentralised economies, and decentralised and decentralised ledgers.

In Lange’s computer socialism, the economy is centralised and the ledger is centralised — the state is a planning machine, both managing the ledger and executing a global plan.

In pre-Marxist communalism, such as the scheme devised by the Welsh utopian socialist Robert Owen, economic planning is centralised but the relevant jurisdiction — that is, the ledger-providing authority — consists of subnational groups of voluntary, socialistic communities.

Hayekian distributed capitalism has a decentralised economy — planning is done by individuals rather than the state — yet the state still organises, records, verifies and updates the ledgers of identities, rights, obligations, and entitlements.

By contrast, in a cryptoeconomy both the economy and the ledgers are decentralised. Blockchains take the state out of both planning and verification.

Information and incentives

Markets work because they align incentives into productive work and they harness distributed information productively.

In the second half of the twentieth century the public choice school extended the incentives critique to encompass the incentives of the planners themselves. How could a socialist commonwealth ensure that planners worked in society’s interest, rather than their own personal interest?

Today, what scholars now call a ‘robust political economy’ (see Mark Pennington’s book and this paper by Peter T. Leeson and J. Robert Subrick) is an economic system structured to deal with the twin problems of information and incentives. How can we coordinate action — make exchanges, build relationships and communities — in a world of incomplete information and potential rentseeking?

Turns out, cryptographers and computer scientists have been working on these two problems as well.

The Byzantine Generals’ Problem

Distributed computing systems have to deal with what is known as the Byzantine Generals’ Problem.

Illustration from the 12th century Madrid Skylitzes, a history of Byzantium between 811 and 1057

The army consists of divisions, each headed up by a general, and they need to establish a consensus about when exactly to launch their attack on the city.

Centralised command is out of the question. No individual general has line of sight to all the generals — or the authority to impose consensus on the whole army at once. They can only communicate by messenger.

So there’s an information problem. The generals need a system — an algorithm — that allows all generals to agree on a consensus.

The problem is made even harder because it’s not certain that all generals are loyal. Some have been paid off by the enemy, and are actively trying to disrupt the plan. The traitorous generals don’t want the loyal generals to come to a consensus.

Thus Byzantine Generals’ Problem describes the challenge of a) achieving consensus in distributed, decentralised systems b) when information flows imperfectly, and c) in the presence of adversaries.

Blockchains achieve Byzantine fault tolerance in part by treating it as an incentive problem. The Bitcoin proof-of-work mechanism incentivises good behaviour, makes it extremely expensive to attack the network, and reduces the payoffs for a successful attack.

The so-called ’51 per cent’ attack on Bitcoin — the possibility that a majority of hashing power could coordinate and then undermine the network — is what would happen if more than half the generals were traitors. (Of course, that itself would be hard to coordinate.)

Two fields together

A decision to attack a city simultaneously is just a narrow slice of the general economic problem: how to coordinate activity in when information is incomplete, communication is imperfect, and people can be lazy, opportunistic, and self-interested.

What computer scientists have been trying to solve algorithmically, economists have been trying to solve constitutionally.

Where cryptographers have found their solutions in public key cryptography and proof of work mechanisms, economists have found solutions in markets, regulation, and institutions.

Blockchains bring these two fields together. They turn constitutional questions into algorithmic questions, and algorithmic questions into constitutional ones.

Byzantine political economy

One way to see this is as a curious historical instance of two largely unrelated fields (computer science and economics) somewhat simultaneously working on a structurally similar problem (decentralised coordination) and arriving at the same type of solutions (consensus protocols and market institutions).

But a more interesting perspective is that blockchain technology actually joins these worlds together in reality. Blockchains can provide the secure fault tolerant decentralised layer for property rights information and its verification and updating whenever that information changes, which can support a decentralised economic layer of markets.

The socialists were wrong in their hopeful quest that (centralised) computers would replace markets. Actually, it is decentralised computers (blockchains) than can replace governments.

Markets always need governance, and the limits of a market society were always the ability of the state to provide those services of record keeping, validation and verification of transactions in property rights. In return, the state levied taxation to fund these services.

Blockchains are a new technology of fault tolerant governance that can furnish the governance to underpin a market economy and society.

We have been asked to make some points about the effect blockchain and similar technologies will have on taxpayer engagement with the taxation system.

The RMIT Blockchain Innovation Hub was established earlier this year as the world’s first social science research centre into the blockchain economy. The Blockchain Innovation Hub will measure and understand the economic, political, social and legal implications of blockchain, and advise governments, firms and communities on how best to take advantage of this exciting new technology.

We’d like to make a few points that we hope might stimulate further discussion and consideration. We are going to be speculative by necessity.

First, this new technology is an opportunity for Australia. We can attract high value knowledge workers by having a competitive tax and regulatory system. Governments should focus on making it easy to host cryptoeconomy services in Australia.

Second, blockchain services are going to change some of the fundamental structures of market capitalism. The twentieth century was dominated by large public companies. In the future, firms will look more like shifting networks managed by blockchains rather than the hierarchies we are used to.

This will have a number of consequences. Australia is heavily reliant on corporate tax revenue. These new firm-like structures are going to be harder to tax than the monolithic firms of the 20th century. We’ve published sceptically about the parliament’s efforts to prevent profit shifting by multinational firms. However, the born-global nature of blockchains will supercharge these trends. We do not believe there will be any easy regulatory solution to this, and parliament will need to rethink not just how it taxes, but what it taxes.

Another consequence of the networked firm is that more people will earn their living as contractors rather than employees. This will have wide-ranging consequences for superannuation, payroll tax, and so on. The tax and industrial relations system has traditionally struggled to integrate contractors into its frameworks, and this is likely to be a bigger issue in the future.

Blockchain applications make possible real-time reporting and payment of tax obligations. A large public company could place its accounts on a publicly verifiable blockchain. This would eliminate the need for auditing.

We are not proposing real time blockchain reporting as a regulatory requirement, but would urge shareholders in public companies to consider demanding this of management.

We can also see some attraction for small and medium sized firms of real time blockchain reporting, which would make automate tax compliance and make business activity statements redundant.

The ATO should develop guidelines for real-time taxpayer blockchain reporting that it would consider compliant. The ATO should also rethink its internal systems to facilitate voluntary real-time reporting.

Real-time tax reporting raises different issues for individual taxpayers. Privacy is an overriding problem here. There are new technologies that have been developed with the blockchain – such as zero-knowledge proofs – that provide opportunities for privacy-protecting public services in the future. This is a something we plan to work on in the future.

Blockchains are likely to bring about enormous changes to the way we work. For now, and to conclude, we will leave it that any use of new digital technology for government revenue raising has to place fundamental values such as privacy and the rule of law at the centre.